ADM 1340 Chapter Notes - Chapter 6: Prope, Britain Yearly Meeting, L Brands

14 Feb 2017

School

Department

Course

Professor

42

ADM 1340 Full Course Notes

Verified Note

42 documents

Document Summary

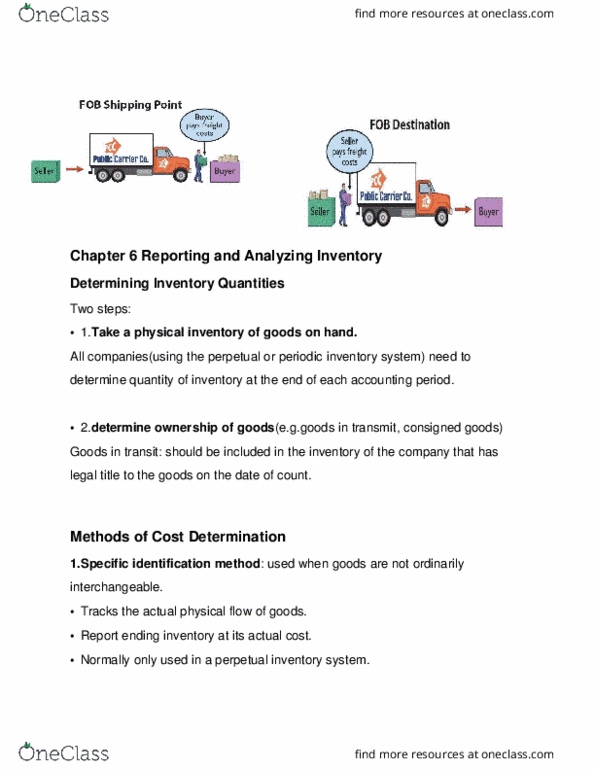

Reporting and analysing inventory: determining inventory quantities, taking a physical inventory, determining ownership of goods. Inventory cost determination methods: specific identification, first-in, first-out (fifo, average cost. Effect of cost determination methods: choice of cost determination method, financial statement effects. Inventory errors: errors made when determining the cost of inventory, errors made when recording the purchase of inventory, presentation and analysis of inventory, valuing inventory at the lower of cost and net realizable value, reporting inventory. Determining inventory quantities: no matter what inventory system companies use, they have to determine their inventory quantities at the end of each accounting period. Since counting should take place in teams of two. This is when the company might have paid for the good, but it still has not arrived: a simple rule should be followed when this happens. Goods in transit should be included in the inventory of the company that has legal title to the goods.