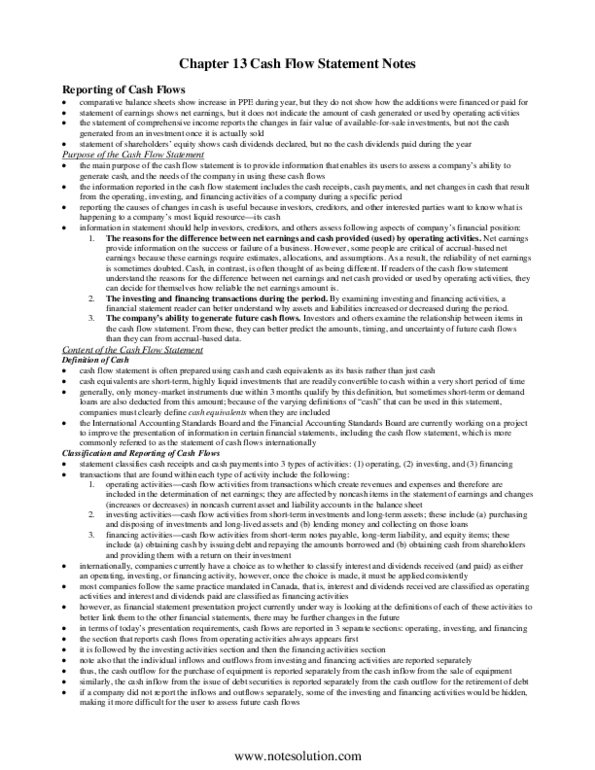

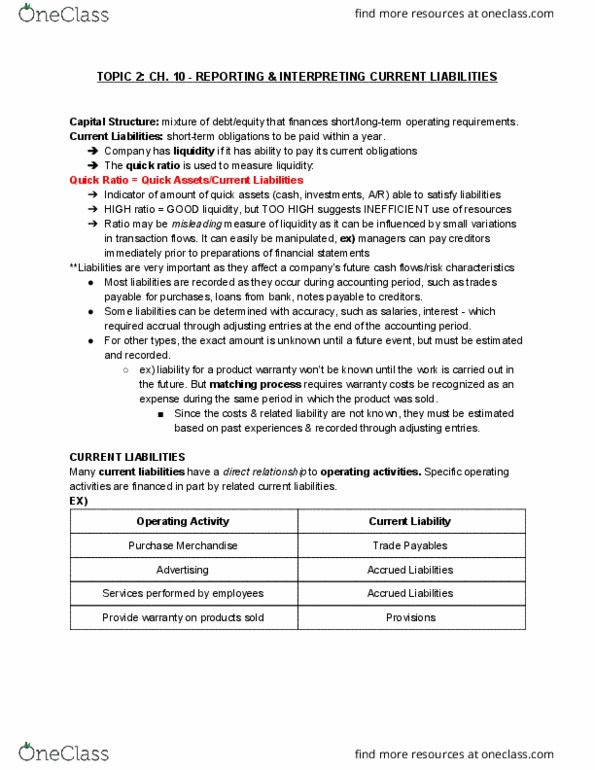

MGAB02H3 Chapter Notes - Chapter 5: Cash Flow, Retained Earnings, Current Liability

Document Summary

Get access

Related Documents

Related Questions

The comparative balance sheet of Cromme Inc. for December 31,2016 and 2015, is shown as follows:

Question not attempted.

1 | Dec. 31, 2016 | Dec. 31, 2015 | |

2 | Assets | ||

3 | Cash | $626,640.00 | $585,760.00 |

4 | Accounts receivable (net) | 226,900.00 | 208,390.00 |

5 | Inventories | 641,350.00 | 616,130.00 |

6 | Investments | 0.00 | 239,300.00 |

7 | Land | 328,730.00 | 0.00 |

8 | Equipment | 705,940.00 | 553,530.00 |

9 | Accumulated depreciation-equipment | (166,970.00) | (148,000.00) |

10 | Total assets | $2,362,590.00 | $2,055,110.00 |

11 | Liabilities and Stockholdersâ Equity | ||

12 | Accounts payable (merchandise creditors) | $425,140.00 | $404,540.00 |

13 | Accrued expenses payable (operating expenses) | 42,020.00 | 52,750.00 |

14 | Dividends payable | 23,580.00 | 19,500.00 |

15 | Common stock, $4 par | 154,000.00 | 100,000.00 |

16 | Paid-in capital: Excess of issue price over parâcommon stock | 416,600.00 | 279,400.00 |

17 | Retained earnings | 1,301,250.00 | 1,198,920.00 |

18 | Total liabilities and stockholdersâ equity | $2,362,590.00 | $2,055,110.00 |

Additional data obtained from an examination of the accounts inthe ledger for 2016 are as follows:

| A. | The investments were sold for $279,880 cash. |

| B. | Equipment and land were acquired for cash. |

| C. | There were no disposals of equipment during the year. |

| D. | The common stock was issued for cash. |

| E. | There was a $198,010 credit to Retained Earnings for netincome. |

| F. | There was a $95,680 debit to Retained Earnings for cashdividends declared. |

Prepare a statement of cash flows, using the indirect method ofpresenting cash flows from operating activities

The section of the statement of cash flows that reports the cashtransactions affecting the determination of net income.

. Refer to the Labels and Amount Descriptions list provided forthe exact wording of the answer choices for text entries. Be sureto complete the heading of the statement. In the operatingactivities section, use the minus sign to indicate cash outflows,decreases in cash and a net cash outflow, if required. In theinvesting and financing activities section, use a minus sign onlyto indicate a NET cash outflow for the section.

| Labels In CengageNOW, a Label is a text entry that does not have anamount associated with it. and Amount DescriptionsIn CengageNOW, an Amount Description is a text entry other thanan Account that has an amount associated with it. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Cash paid for dividends | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Cash paid for merchandise | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Cash paid for purchase of equipment | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Cash paid for purchase of land | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Cash received from customers | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Cash received from sale of common stock | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Cash received from sale of investments | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| December 31, 2016 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Decrease in accounts payable | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Decrease in accounts receivable | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Decrease in accrued expenses payable | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Decrease in inventories | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Decrease in cash | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Depreciation | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| For the Year Ended December 31, 2016 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Gain on sale of investments | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Increase in accounts payable | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Increase in accounts receivable | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Increase in accrued expenses payable | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Increase in cash | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Increase in inventories | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Loss on sale of investments | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Net cash flow from operating activities | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Net cash flow used for operating activities | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Net cash flow from investing activities | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Net cash flow used for investing activities | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Net cash flow from financing activities | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Net cash flow used for financing activities | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Net income Prepare a statement of cash flows, using the indirect method ofpresenting cash flows from operating activities The section of the statement of cash flows that reports the cashtransactions affecting the determination of net income. . Refer to the Labels and Amount Descriptions list provided forthe exact wording of the answer choices for text entries. Be sureto complete the heading of the statement. In the operatingactivities section, use the minus sign to indicate cash outflows,decreases in cash and a net cash outflow, if required. In theinvesting and financing activities section, use a minus sign onlyto indicate a NET cash outflow for the section. Question not attempted.

|

urgent need it an hour wil rate

The comparative balance sheets of Posner Company, for Years 1 and 2 ended December 31, appear below in condensed form.

| 1 | Year 2 | Year 1 | |

| 2 | Cash | $53,000.00 | $50,000.00 |

| 3 | Accounts Receivable (net) | 37,000.00 | 48,000.00 |

| 4 | Inventories | 108,500.00 | 100,000.00 |

| 5 | Investments | 70,000.00 | |

| 6 | Equipment | 573,200.00 | 450,000.00 |

| 7 | Accumulated Depreciation-Equipment | (142,000.00) | (176,000.00) |

| 8 | $629,700.00 | $542,000.00 | |

| 9 | Accounts Payable | $62,500.00 | $43,800.00 |

| 10 | Bonds Payable, Due Year 2 | 100,000.00 | |

| 11 | Common Stock, $10 par | 325,000.00 | 285,000.00 |

| 12 | Paid-In Capital in Excess of ParâCommon Stock | 80,000.00 | 55,000.00 |

| 13 | Retained Earnings | 162,200.00 | 58,200.00 |

| 14 | $629,700.00 | $542,000.00 |

The income statement for the current year is as follows:

| 1 | Sales | $625,700.00 | |

| 2 | Cost of merchandise sold | 340,000.00 | |

| 3 | Gross profit | $285,700.00 | |

| 4 | Operating expenses: | ||

| 5 | Depreciation expense | $26,000.00 | |

| 6 | Other operating expenses | 68,000.00 | 94,000.00 |

| 7 | Income from operations | $191,700.00 | |

| 8 | Other revenue and expense: | ||

| 9 | Gain on sale of investment | $4,000.00 | |

| 10 | Interest expense | (6,000.00) | (2,000.00) |

| 11 | Income before income tax | $189,700.00 | |

| 12 | Income tax | 60,700.00 | |

| 13 | Net income | $129,000.00 |

Additional data for the current year are as follows:

| (a) | Fully depreciated equipment costing $60,000 was scrapped, no salvage, and new equipment was purchased for $183,200. |

| (b) | Bonds payable for $100,000 were retired by payment at their face amount. |

| (c) | 5,000 shares of common stock were issued at $13 for cash. |

| (d) | Cash dividends declared and paid, $25,000. |

Required:

| Prepare a statement of cash flows using the indirect method of reporting cash flows from operating activities. Refer to the Labels and Amount Descriptions list provided for the exact wording of the answer choices for text entries. Be sure to complete the heading of the statement. Use the minus sign to indicate cash outflows, cash payments, decreases in cash, or any negative adjustments. |

Labels and Amount Descriptions

| Labels | |

| For the Year Ended December 31, Year 2 | |

| Amount Descriptions | |

| Cash from sale of common stock | |

| Cash from sale of investments | |

| Cash paid for dividends | |

| Cash paid for purchase of equipment | |

| Cash paid to retire bonds payable | |

| Decrease in accounts payable | |

| Decrease in accounts receivable | |

| Decrease in cash | |

| Decrease in inventories | |

| Depreciation | |

| Gain on sale of investment | |

| Increase in accounts payable | |

| Increase in accounts receivable | |

| Increase in cash | |

| Increase in inventories | |

| Loss on sale of investment | |

| Net cash flow from financing activities | |

| Net cash flow from investing activities | |

| Net cash flow from operating activities | |

| Net cash flow used for financing activities | |

| Net cash flow used for investing activities | |

| Net cash flow used for operating activities | |

| Net income | |

| Net loss |

Statement of Cash Flows

Prepare a statement of cash flows using the indirect method of reporting cash flows from operating activities. Refer to the Labels and Amount Descriptions list provided for the exact wording of the answer choices for text entries. Be sure to complete the heading of the statement. Use the minus sign to indicate cash outflows, cash payments, decreases in cash, or any negative adjustments.

| Posner Company |

| Statement of Cash Flows |

| 1 | Cash flows from operating activities: | ||

| 2 | |||

| 3 | Adjustments to reconcile net income to net cash flow from operating activities: | ||

| 4 | |||

| 5 | |||

| 6 | Changes in current operating assets and liabilities: | ||

| 7 | |||

| 8 | |||

| 9 | |||

| 10 | |||

| 11 | Cash flows from investing activities: | ||

| 12 | |||

| 13 | |||

| 14 | |||

| 15 | Cash flows from financing activities: | ||

| 16 | |||

| 17 | |||

| 18 | |||

| 19 | |||

| 20 | |||

| 21 | Cash at the beginning of the year | ||

| 22 | Cash at the end of the year |