RSM219H1 Chapter Notes -Interest Expense, Net Income, Tax Deduction

7

RSM219H1 Full Course Notes

Verified Note

7 documents

Document Summary

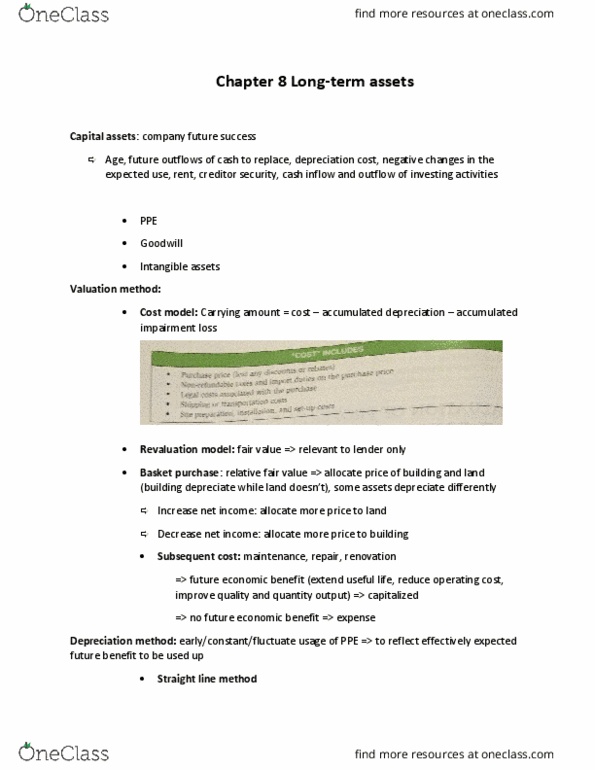

Includes: land, real estate, buildings, equipment, vehicles, computers, patents, and so on that companies need to carry out operations. Requires a substantial mortgages or debt to finance them. Users anticipate the future outflows of cash to replace them. Methods a company uses to depreciate its assets (on statement of earnings) The original cost is recorded at the time of acquisition. When it is used, its cost is expensed using a depreciation method. M. v. is only recognized when it is sold. Gain or loss on sale depends on the difference between the proceeds form the sale and the net book value at the time of sale. Net book value/ carrying value/ depreciation cost is the original cost less the portion that has been charged to expense in the form of depreciation: market value, replacement cost (buy) The amount that would be needed to acquire an equivalent asset. Replacement cost and the depreciation expense have a positive relationship.