RSM219H1 Chapter Notes - Chapter 3: General Ledger, Template Method Pattern, Book Value

7

RSM219H1 Full Course Notes

Verified Note

7 documents

Document Summary

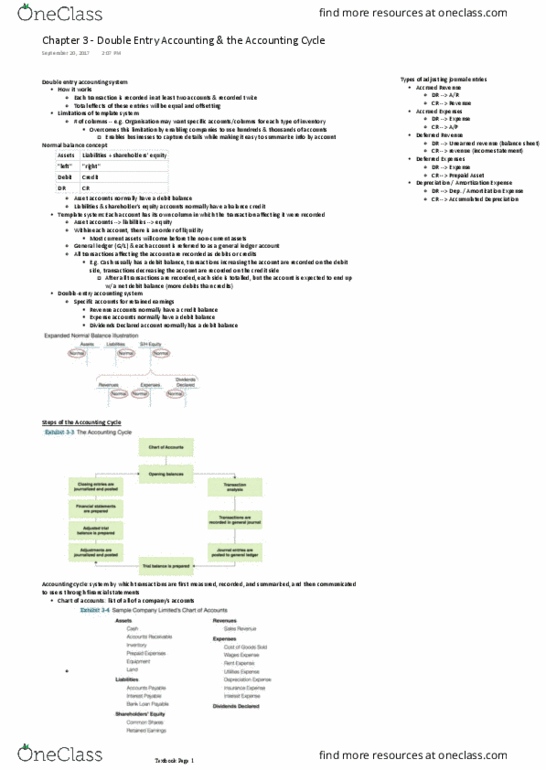

Chapter 3: double-entry accounting and the accounting cycle. Requires that each transaction be recorded in a way that affects at least two accounts. With this you can put as many entries as you want. The amount of columns that can be manageably used. Using this concept, you can determine whether an account normally has a debit or credit balance. The accounts are put in order of liquidity. All the accounts are in the general ledger. A list of all the (cid:272)o(cid:373)pa(cid:374)(cid:455)"s a(cid:272)(cid:272)ou(cid:374)ts. Permanent account can be changed whenever, but not temporary accounts. I(cid:374)(cid:272)ludes: assets, lia(cid:271)ilities, sha(cid:396)eholde(cid:396)"s e(cid:395)uit(cid:455), (cid:396)eve(cid:374)ues, e(cid:454)pe(cid:374)ses, divide(cid:374)ds de(cid:272)la(cid:396)ed: opening balances. Temporary accounts always get reset and start from 0. Permanent accounts have a carrying balance: transaction analysis. Identifying whether an event or transaction has occurred and it so determining its effect on the (cid:272)o(cid:373)pa(cid:374)(cid:455)"s a(cid:272)(cid:272)ou(cid:374)ts. Source document evidence that a transaction occurred. Invoices, cheques, cash register tapes, bank deposits slips: transactions recorded in the general journal.