RSM220H1 Chapter Notes - Chapter 4: Cash Flow Statement, Retained Earnings, Earnings Management

Document Summary

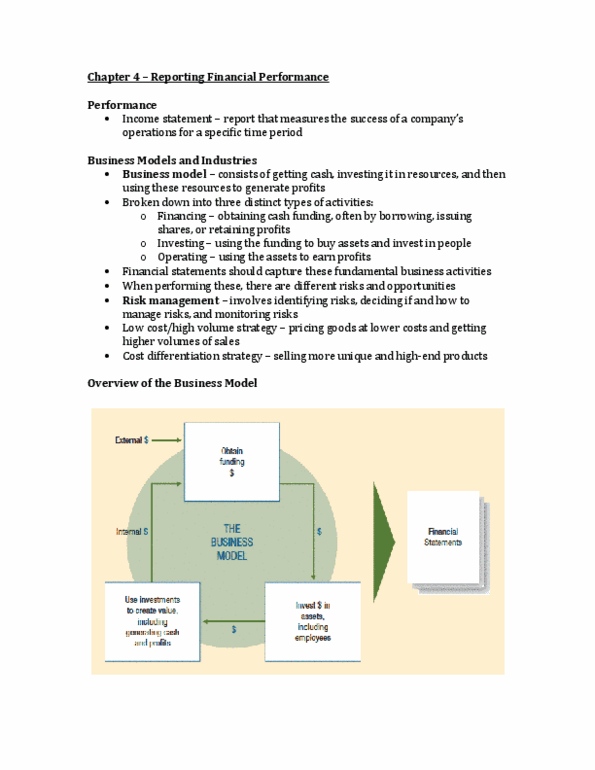

All business is based on the business model of getting $, investing it in resources, and then using these resources to generate profits: model can be broken down into 3 types of activities: Financing: obtaining $ funding, by borrowing, issuing shares, or retaining profits; also involve the repayment of debt or repurchase of shares. Investing: using the funding to buy assets and invest in ppl; these also include divestitures. Operating: using the assets and ppl to earn profits. Value creation is central in any business model- need to max shareholder value. Therefore fs should capture these fundamental business activities and communicate them properly: how info is communicated: Bs: aims to capture the financing and investing activities. Is: captures o and performance related activities. Cash flow statement: looks at interrelationship btwn activities. Is is the report that measures the success of a companys operations for a specific time period. Ppl use this report to determine profitability, investment value, and creditworthiness.