RSM324H1 Chapter 4: CHAPTER 4-2

15 Feb 2017

School

Department

Course

Professor

Document Summary

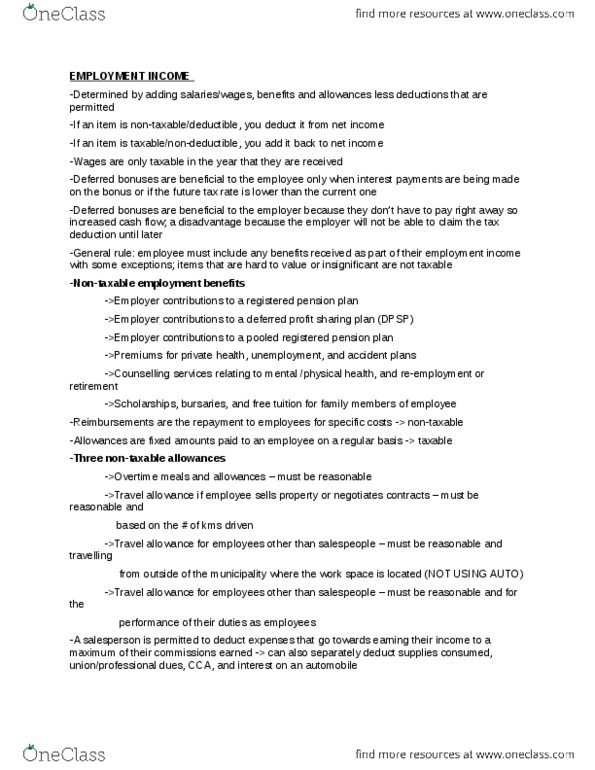

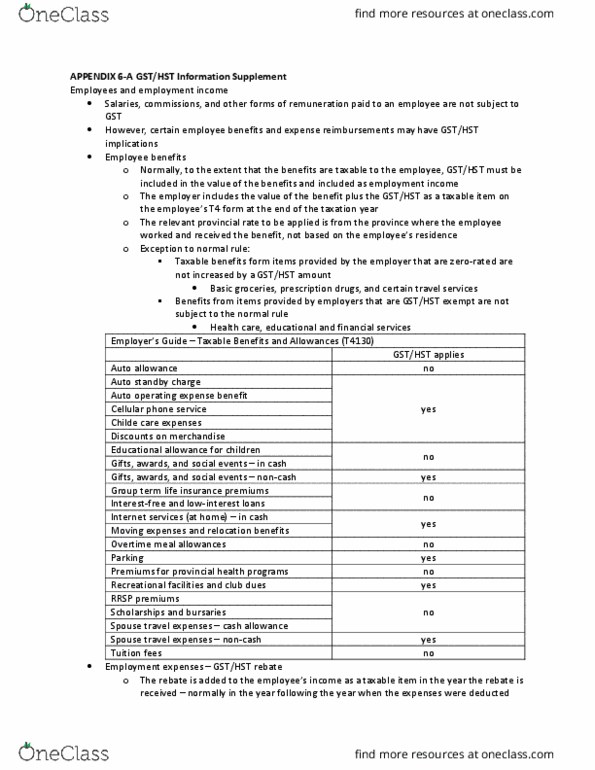

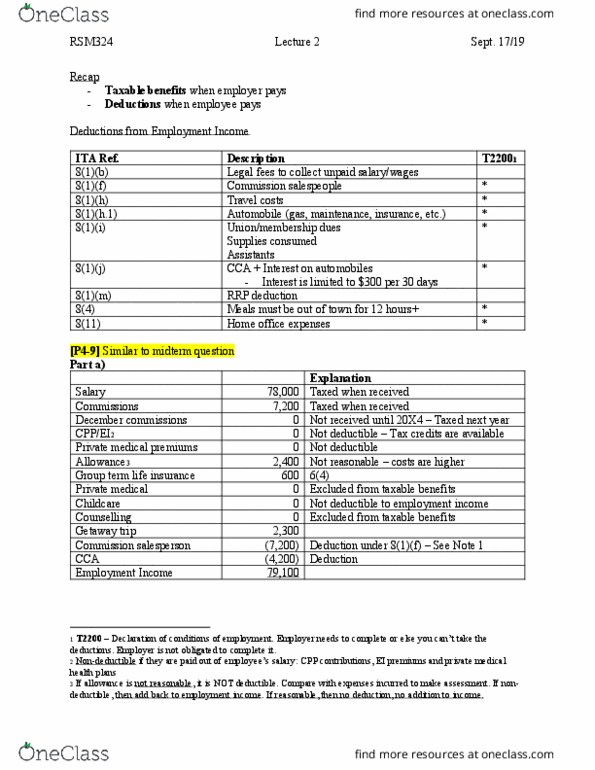

Exceptions: overtime meals and allowances: reasonable (up to /meal) Reaso(cid:374)a(cid:271)le o(cid:448)erti(cid:373)e (cid:373)eal allo(cid:449)a(cid:374)(cid:272)es are not ta(cid:454)a(cid:271)le if: (cid:862)the e(cid:373)plo(cid:455)ee (cid:449)orks. 2 or more hours of overtime right after the scheduled hours of work; and the overtime is infrequent and occasional in nature (< 3 times a (cid:449)eek(cid:895)(cid:863) Tra(cid:448)el e(cid:454)pe(cid:374)ses: tra(cid:374)sportatio(cid:374) (cid:894)(cid:272)ar, pla(cid:374)e, (cid:895), (cid:373)eals, lodgi(cid:374)g, a(cid:374)d other incidental costs. If allowance is unreasonably high or low in relation to the actual costs incurred, the allowance is taxable, and expenses can be deducted. Tax-free car allowance if reasonable and based on #km used to conduct employment duties. Tax-free allowance eliminates the right to claim expenses that would otherwise be permitted. If the allowance is considered tax-free, the employee cannot claim certain expenses that are specifically permitted: employees other than salespeople (regular employees): entitled to receive a tax-free allowance for travel expenses (however, more extensive criteria than for salespeople)