RSM423H1 Chapter Notes - Chapter 15: Contingent Liability, Internal Control, Accounts Receivable

Document Summary

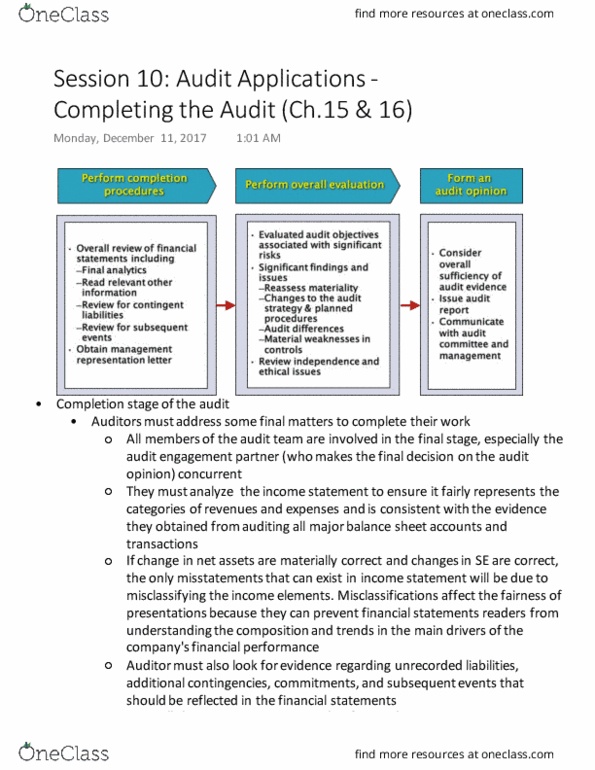

This chapter covers completion of the financial statement audit. Audit of the nominal or flow accounts cannot be completed until year end. Audit of several year-end balances has been covered in auditing the accounting cycles. Some procedures are particular to year end such as subsequent events, contingencies, presentations, and disclosures. Final wrap-up of the audit is also discussed. A number of the revenue and related topics were audited in whole or in part with other related account groups. Working papers should show cross-reference indexing to the revenue and expense accounts in the trial balance. Some minor expense accounts like office supplies or utilities will not be covered until the end of the audit. Auditors usually apply analytical procedures to these accounts. All miscellaneous accounts and clearing accounts with debit balances are analyzed. Accounts with income tax implications are also analyzed carefully. Analytical procedures can be used at all points of the audit.