Management and Organizational Studies 1023A/B Chapter Notes - Chapter 5: Questioned Document Examination, Modus Operandi, Forensic Accounting

1 Aug 2015

School

Department

Professor

9

MOS 1023A/B Full Course Notes

Verified Note

9 documents

Document Summary

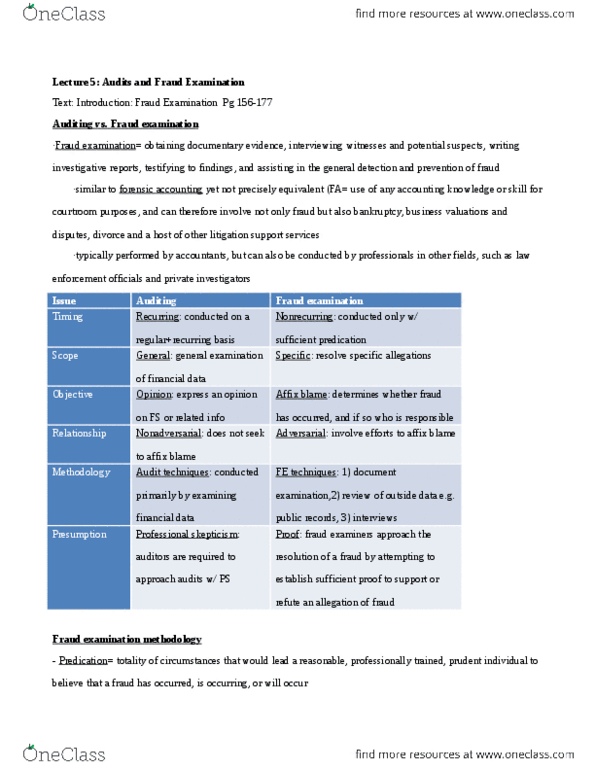

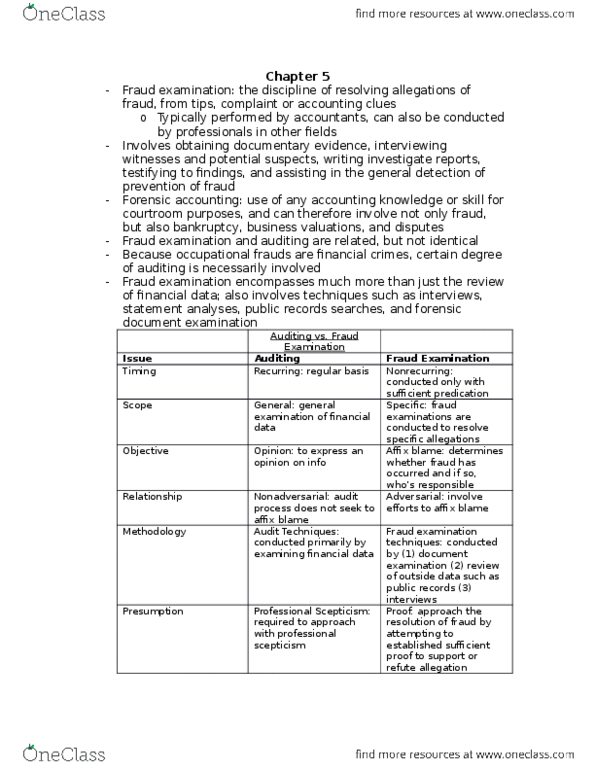

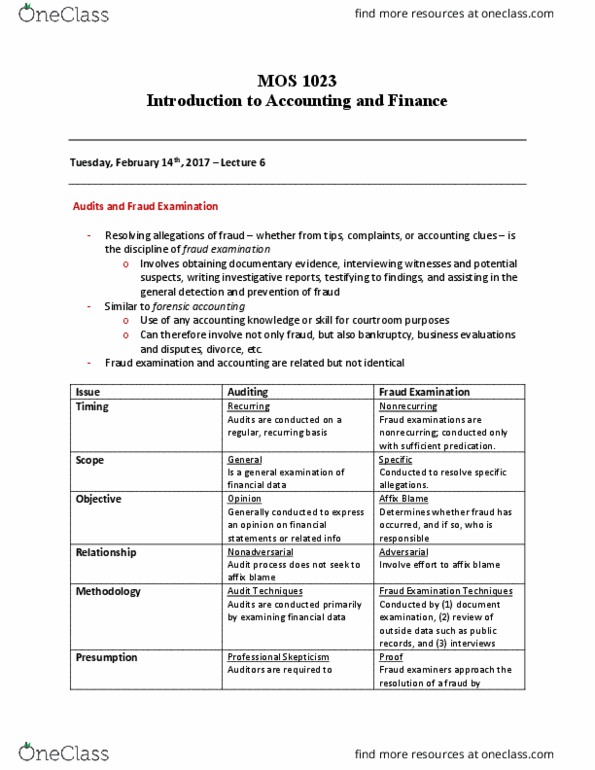

Introduction to mos 1023 - audits and frauds: fraud examination resolving allegations of fraud. Audits are conducted on a regular, recurring basis. The audit is a general examination of financial data. An audit is generally conducted to express an opinion on financial statements or related information. The audit does not seek to affix blame. Audits are conducted primarily by examining financial data. Fraud examinations are conduced to resolve specific allegations. The fraud examination determines if fraud has occurred, and if so, who is responsible. Fraud examinations are conducted by 1) document examination, 2) review of outside data such as public records, 3) interviews. Fraud examiners approach the resolution of a fraud by attempting to establish sufficient professional skepticism proof to support or refute an allegation of fraud. Internal fraud offences committed by people who work for organizations, most costly and common. Learning of criminal activity usually occurred within intimate personal groups attitudes, drives, rationalizations, and motives of the criminal mind.