BU127 Chapter Notes - Chapter 4: Accrual, Historical Cost, Debits And Credits

6

BU127 Full Course Notes

Verified Note

6 documents

Document Summary

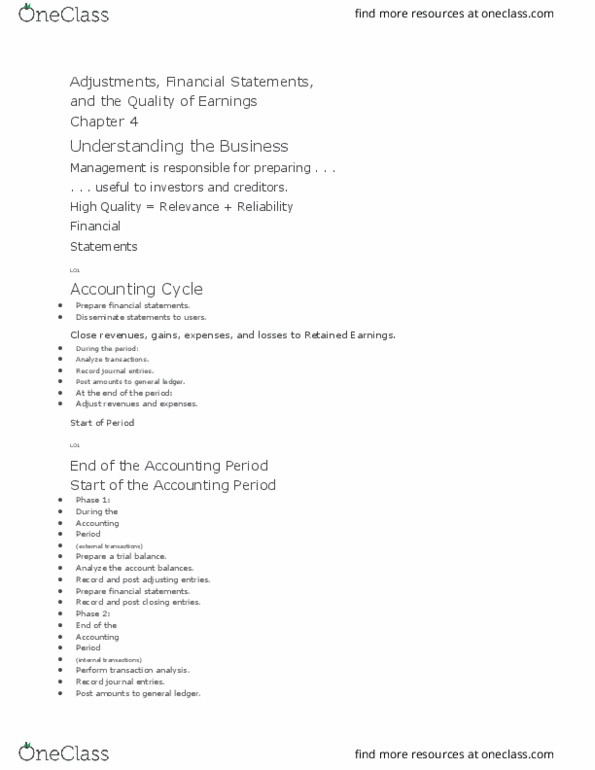

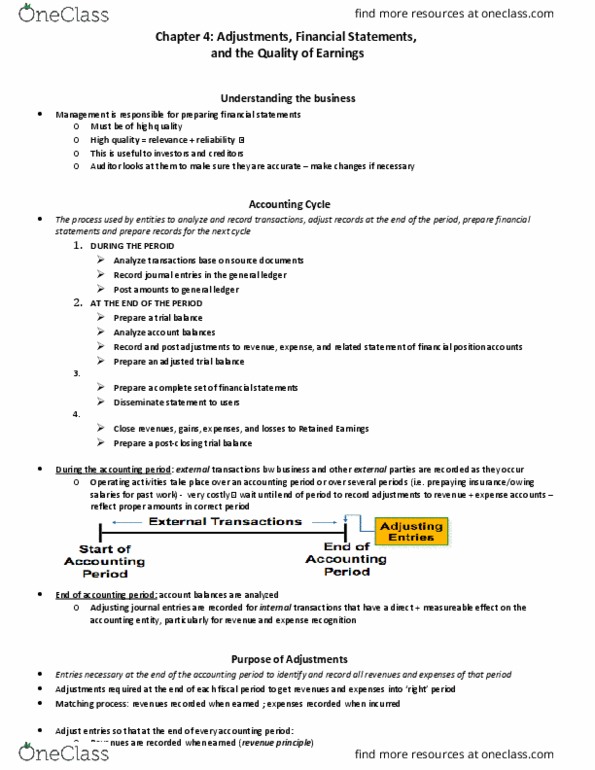

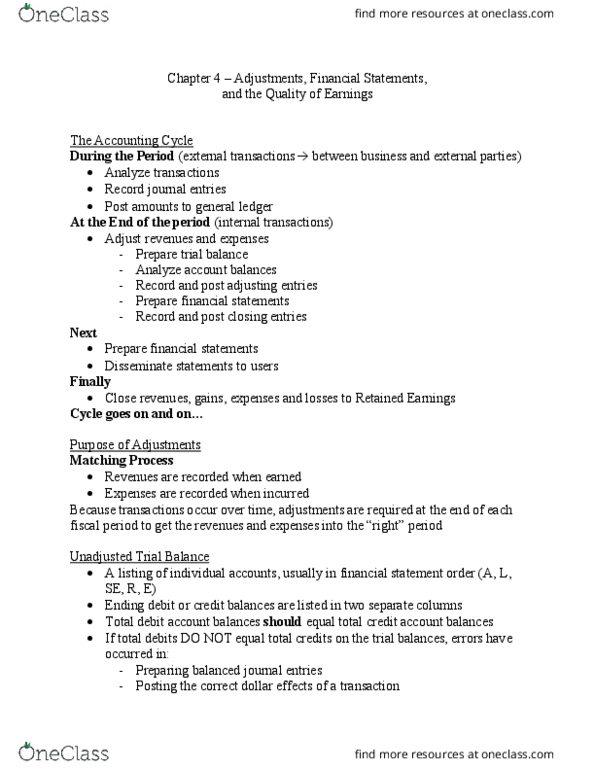

Chapter 4: adjustments, financial statements, and the quality of earnings. Disseminate statements to: close revenues, gains, expenses, and losses to retained earnings. Cash is not always received in the period in which the company earns revenue; likewise, cash is not always paid in the period in which the company incurs an expense. In this case, adjusting entries are being used. Adjusting entries are entries necessary at the end of the accounting period to identify and record all revenues and expenses of that period, so that. Revenues are recorded when earned (the revenue principle) Expenses are recorded when they are incurred to generate revenue during the same period (the matching process) Assets are reported at amounts that represent the probable future benefits remaining at the end of the period. Liabilities are reported at amounts that represent the probable future sacrifices of assets or services owed at the end of the period.