BU247 Chapter Notes - Chapter 3: Sunk Costs, Opportunity Cost, Cost Driver

Document Summary

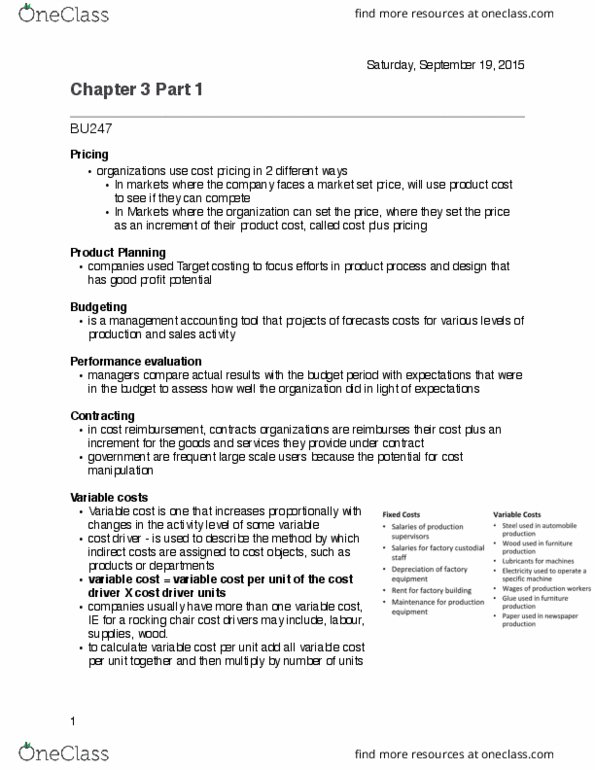

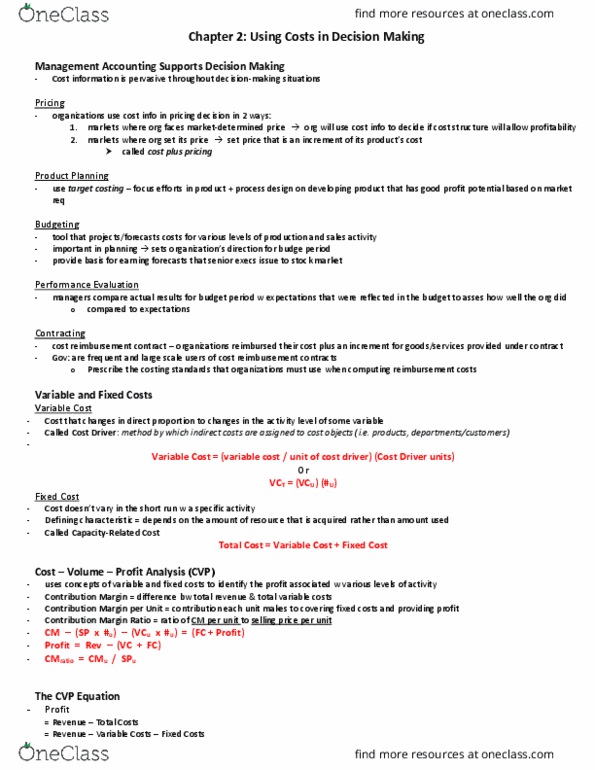

Organizations use cost information in the pricing decision in two ways. In markets where the organization faces a market-determined price, the organization will use product cost information to decide whether its cost structure will allow it to compete profitably. In markets where the organization can set its price, organizations will often set a price that is an increment of its product cost an approach called cost plus pricing. Organizations use a tool called target costing to focus efforts in product and process design on developing a product that has a good profit potential in view of market requirements. Projects or forecasts costs for various levels of production and sales activity. Managers compare the actual results from the budget period with expectations that were reflected in the budget to assess how well the organization did in light of its expectations. Organizations are reimbursed their cost plus an increment for the goods or services they provide under the contract.