BU247 Chapter Notes -Sunk Costs, Cost Driver, Marginal Cost

Document Summary

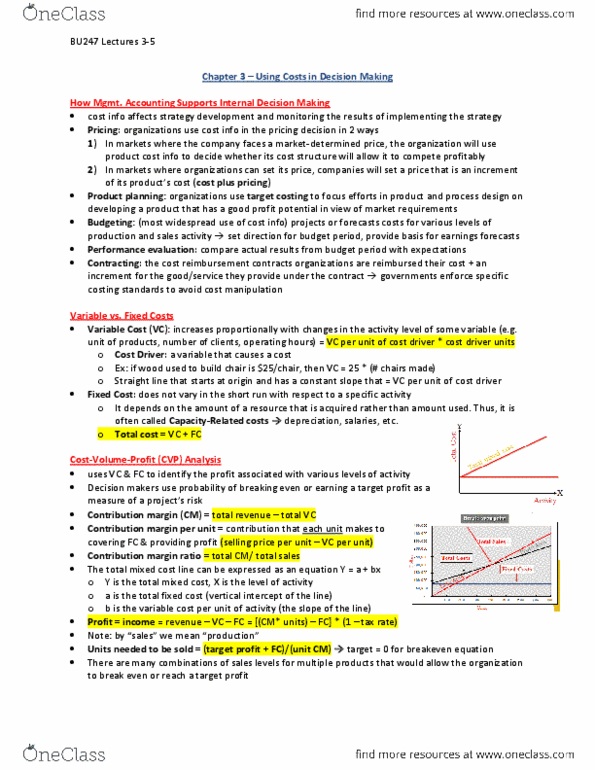

Chapter 3 using costs in decision making. Product planning: organizations use target costing to focus efforts in product and process design on developing a product that has a good profit potential in view of market requirements. Budgeting: (most widespread use of cost info) projects or forecasts costs for various levels of production and sales activity set direction for budget period, provide basis for earnings forecasts. Performance evaluation: compare actual results from budget period with expectations. Contracting: the cost reimbursement contracts organizations are reimbursed their cost + an increment for the good/service they provide under the contract governments enforce specific costing standards to avoid cost manipulation. Fixed cost: does not vary in the short run with respect to a specific activity. It depends on the amount of a resource that is acquired rather than amount used. Thus, it is often called capacity-related costs depreciation, salaries, etc: total cost = vc + fc.