BU353 Chapter Notes - Chapter 18: Home Insurance, Commercial Property, Property Insurance

Document Summary

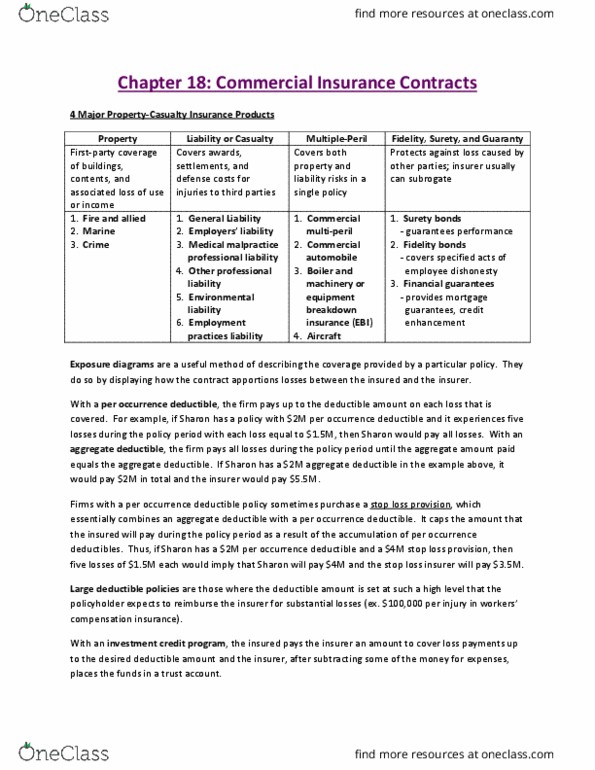

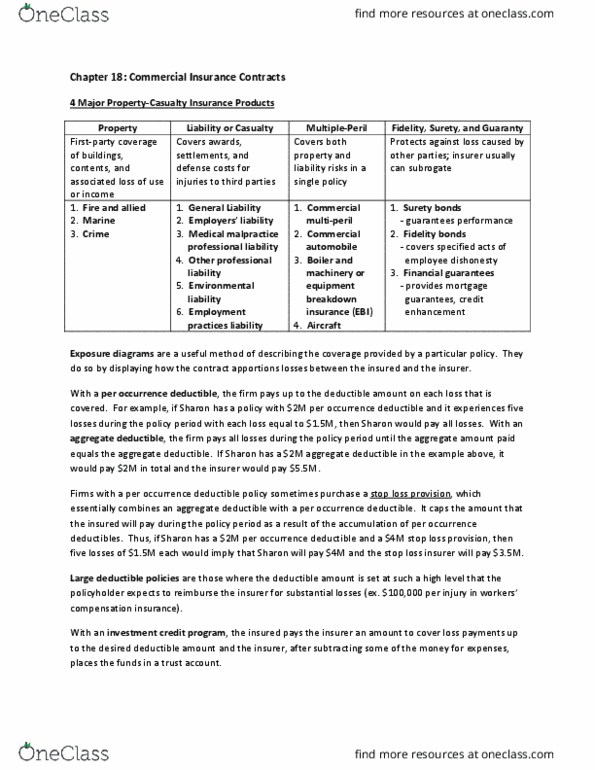

Commercial insurance contracts are broadly classified as either property-casualty or life-health- retirement contracts. The latter classification includes group life, medical, disability, annuity, and related pension contracts associated with employee benefit plan, as well as corporate-owned life insurance on key personnel and other employees. Businesses often retain substantial amounts of loss and/or rely on alternative risk transfer devices where the costs are not reflected in commercial lines insurance premiums. The largest two commercial lines of business are general liability which covers liability arising out of common business hazards, and commercial property. Separate policies and hundreds of endorsements are available to customize contracts, either by adding coverage for a higher premium, or deleting coverage for a premium reduction. Larger business buyers often negotiate customized terms of coverage to meet special needs. Highly customized contracts often are called manuscript policies. Policy standardization facilitates price and service comparisons among insurers by risk managers, brokers, and other commercial insurance buyers.