BU477 Chapter Notes - Chapter 6: Audit Risk, Human Capital, Engagement Letter

Document Summary

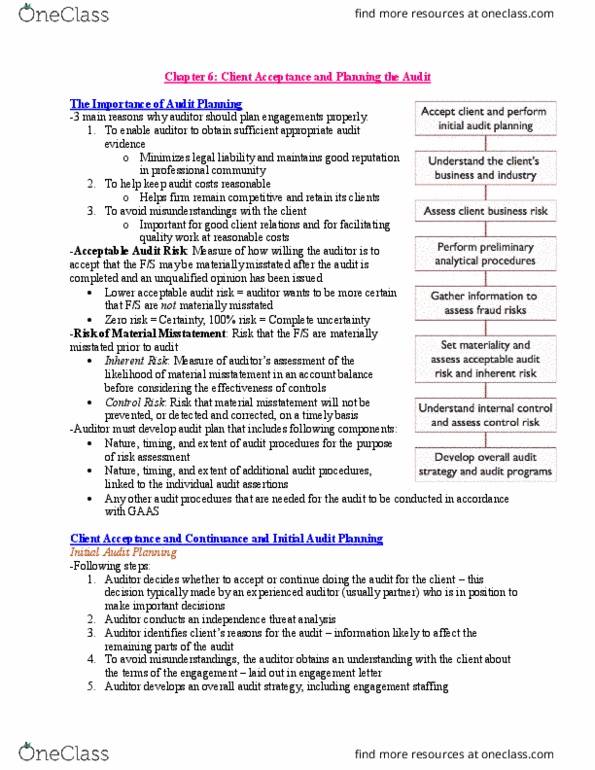

Planning is to provide for effective conduct of the audit: To enable the auditor to obtain sufficient appropriate audit evidence: 2. To help keep audit costs reasonable: 3. Acceptable audit risk: a measure of how willing the auditor is to accept that the financial statements may be materially misstated after the audit is completed and an unqualified opinion has been issued. Risk of material misstatement: the risk that the financial statements are materially misstated prior to audit, control risk: The risk that material misstatement will not be prevented or detected and corrected on a timely basis. Client acceptance and continuance and initial audit planning. Auditor decides whether to accept or continue doing the audit for the client. This decision is typically made by an experienced auditor (partner) who is in a position to make important decisions: 2. Auditor conducts an independence threat analysis: 3. Auditor identifies the client"s reasons for the audit.