BU477 Chapter Notes - Chapter 4: Market Capitalization, Audit Evidence, Confirmation Bias

Document Summary

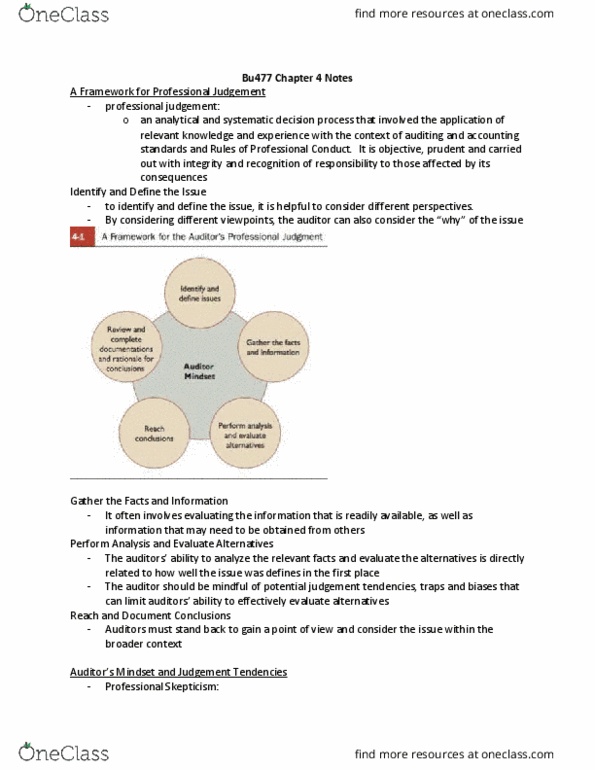

Professional judgment: analytical and systematic decision process that involves the application of relevant knowledge and experience with the context of auditing and accounting standards and rules of professional conducts. Is objective, prudent, and carried out with integrity and recognition of responsibility to those affected by its consequences. Framework for auditor"s professional judgment effective in guiding thinking and encouraging auditors to be aware of their own judgment biases and traps and what can go wrong. Framing the problem : must be clear about what to solve. To help identify and define the issue: consider different perspectives helps auditor focus on real issue and why" more likely to apply appropriate professional skepticism. Helps auditors to avoid judgment trap of rushing to solve the problem important since auditors face considerable time pressures and may be too quick in accepting evidence and mgmt. "s explanations. Evaluating the information that"s readily available, and information that may be obtained from others.