BU487 Chapter Notes - Chapter 6: Retained Earnings, Consolidated Financial Statement, Promissory Note

Document Summary

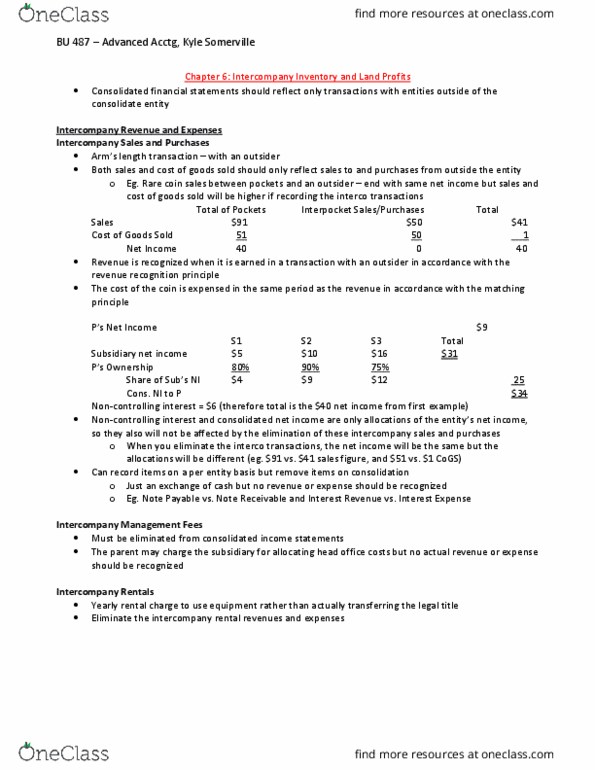

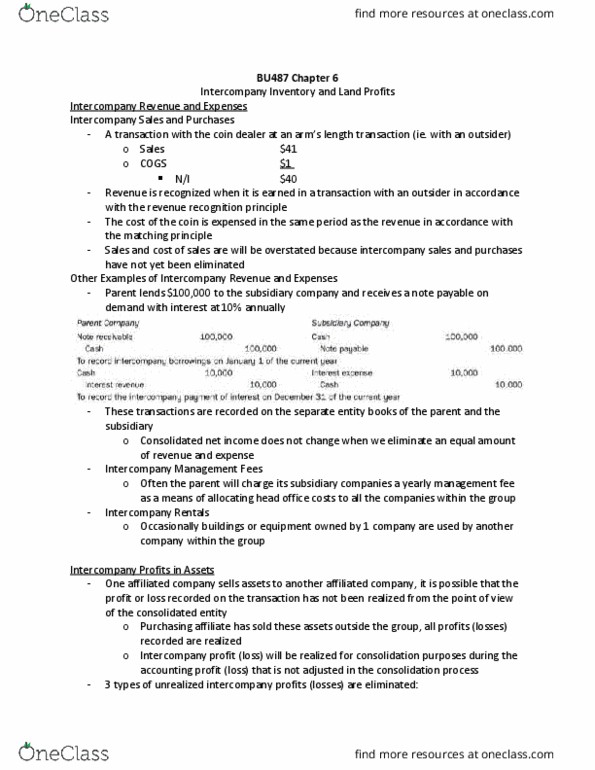

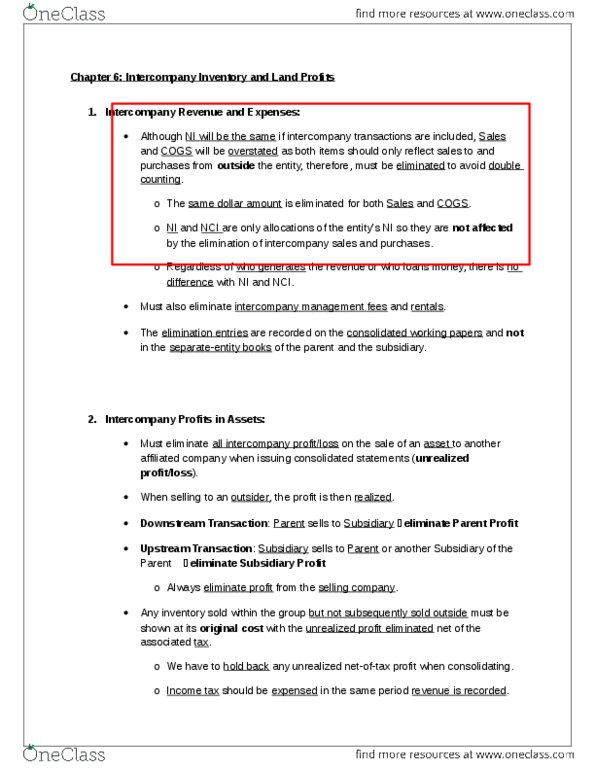

Vertically integrated chain of organizations reduces their costs and risks by affiliating within each other. Consolidated financial statements should reflect transactions with entities outside of consolidated entity. Intercompany can be shifting income from one company to another to minimize taxes. Transaction needs to be with someone arms-length outsider. The best way of determining the intercompany net income is by adding the sums of each company"s net income. Example: there can be four pockets and in each pocket it generates a different amount of net income, to determine the interpocket income on the consolidated financial statement you would add all the pockets. These steps are repeated for all net income properties (sales and cost of goods sold) If we take the total pocket and eliminate the interpocket transactions, we will be left with the consolidated values. If there is a percentage of net income, then apply that when calculating the consolidated net income.