BUS-A 201 Chapter Notes - Chapter 3: Income Statement

Document Summary

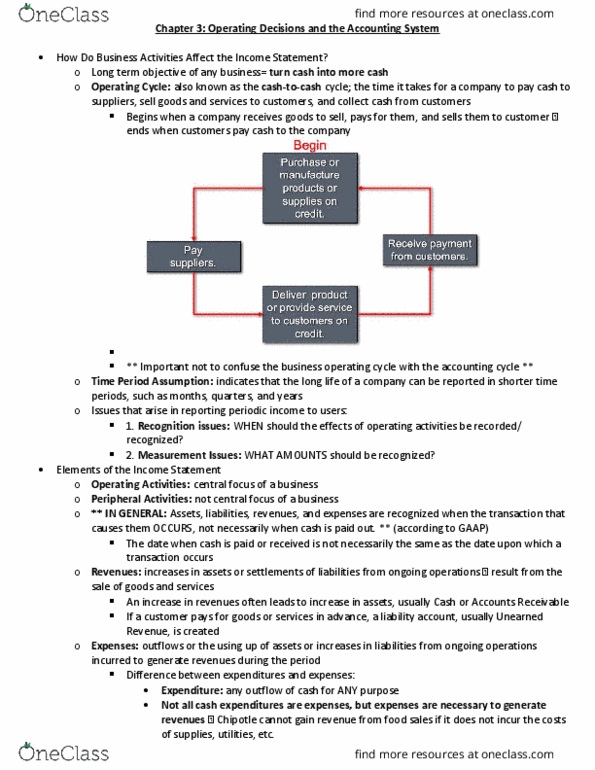

Operating (cash to cash cycle) example: purchases goods and services on a credit, pay cash to suppliers, sells goods and services to customers, receive cash from customers. Long life of a company can be reported in shorter time periods. Peripheral activities: not central focus for business. Increases in assets or settlements of liabilities from the major or central ongoing operations of the business. Outflows or the using up of assets or increases in liabilities from ongoing operations incurred to generate revenue. Revenues are recorded when cash is received and expenses are recorded when cash is paid. When the company transfers promised goods or services to customers. Requires that costs incurred to generate revenues be recognized in the same period; a matching costs with benefits. Assets, liabilities, stockholders" equity, revenues, and expenses. Amounts the company expects to collect for previous credit sales.