MGMT 30A Chapter Notes - Chapter 4: Earnings Management, Uptodate, Historical Cost

7

MGMT 30A Full Course Notes

Verified Note

7 documents

Document Summary

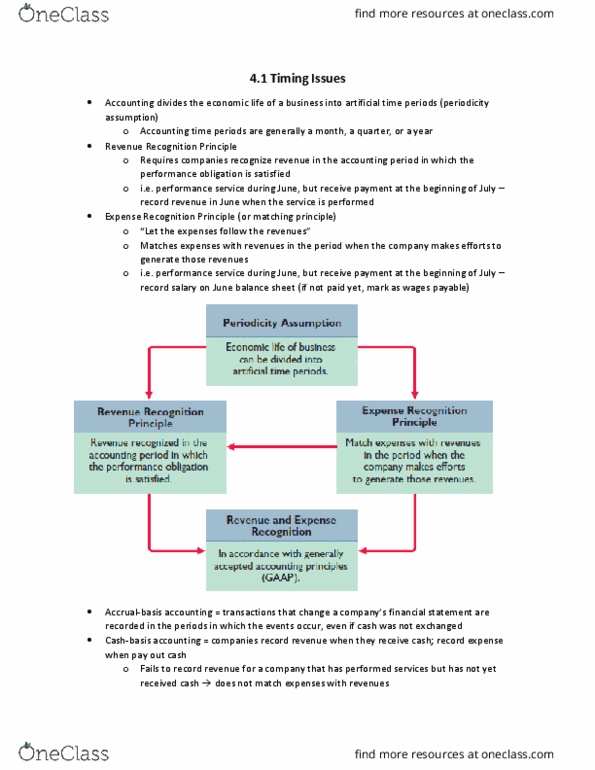

Accounting divides the economic life of a business into artificial time periods (month, quarter, year) Accrual method: recognizes transactions in the period they are incurred, irrespective of when cash is exchanged. Revenue recognition principle: requires companies to recognize revenue in the accounting period in which the performance obligation is satisfied (recognize revenues in the period they are earned) Expense recognition (matching) principle: match expenses with revenues in the period when the company makes efforts to generate those revenues (recognize expense in period thy are incurred to generate revenue) 4 type of adjusting entries: prepaid expenses (prepayments): expenses paid in cash and recorded as assets before they are used or consumed, cash paid before expenses incurred. Involves adjusting assets for consumption (recognizing expenses): prepaids, supplies, p, p&e for depreciation: unearned revenues: revenues received in cash and recorded as liabilities before they are earned, cash received before revenue is earned.