COMMERCE 1AA3 Lecture Notes - Lecture 5: Matching Principle, Accrual, Installment Sale

23 Feb 2017

School

Department

Course

Professor

Document Summary

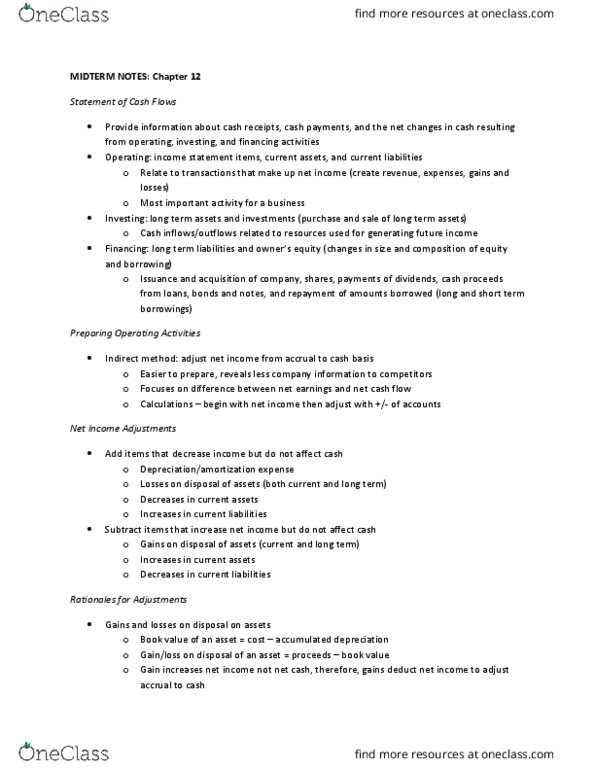

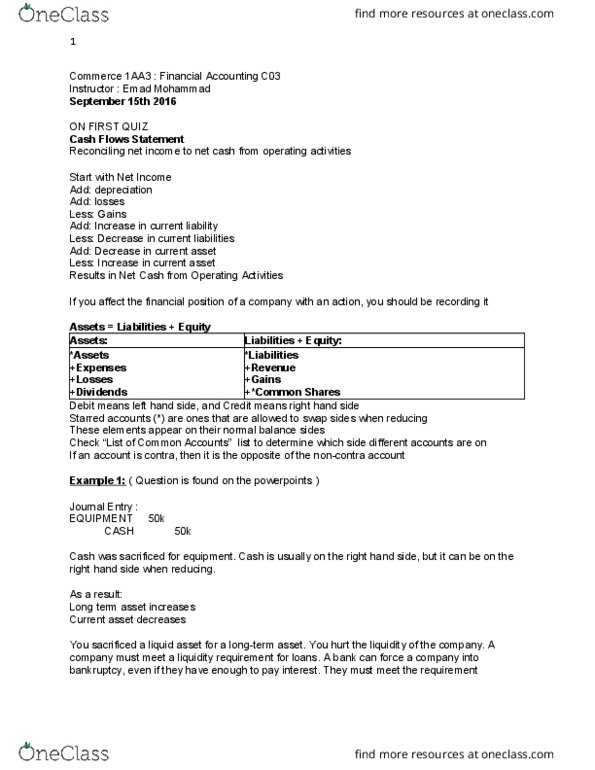

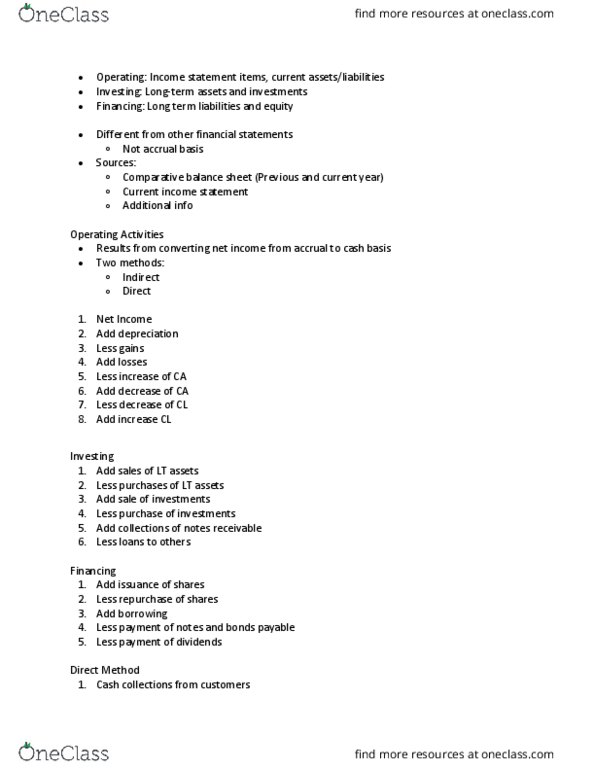

**note: adjustments to reconcile net income to net cash operating activities (below) Net cash from operating activities xx xx (xx) xx xx (xx) (xx) xx single underline xx double underline. Record anything that affects the financial position of a company, aka assets, liabilities and equity. Retained earnings is net income dividends. Net income is revenue + gain losses - expenses. Asset + expenses + losses + dividends = liabilities + revenues + gains + common shares. The (cid:449)ay they appear is (cid:272)alled (cid:862)normal balance(cid:863)! (cid:894)(cid:271)elo(cid:449)(cid:895) Lhs(left hand side) (debit dr) rhs(right hand side) of account. **** = 3 items that are allowed to swap sides when reducing. Slide 14 transaction: hurt liquidity of the company by trading a long-term asset for a short- term asset. Slide 15 transaction: increase current assets by 3000, therefore revenue is increased by 3000, therefore, net income increased by 3000 retained earnings (r/e) + 3000 equity + 3000 .