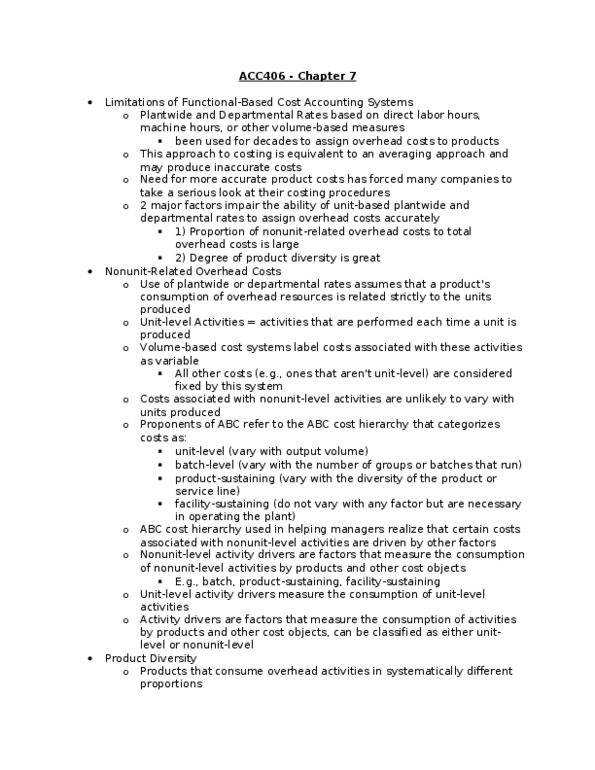

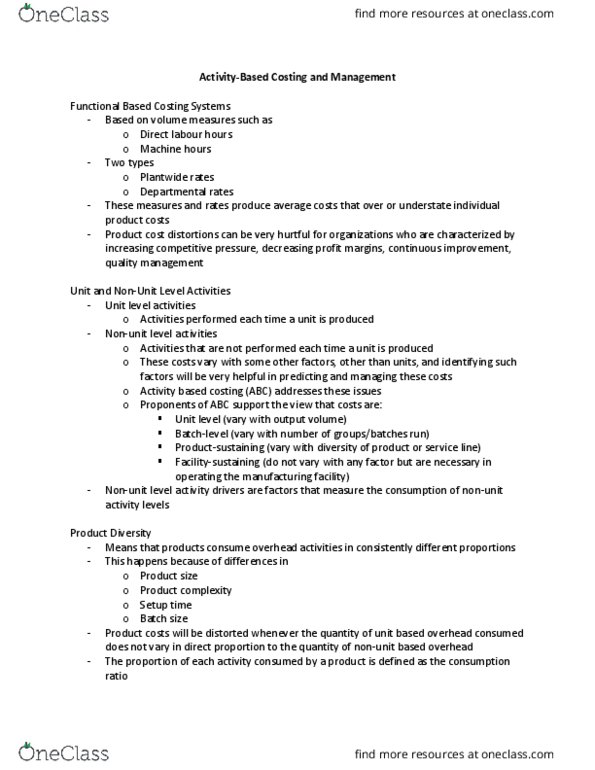

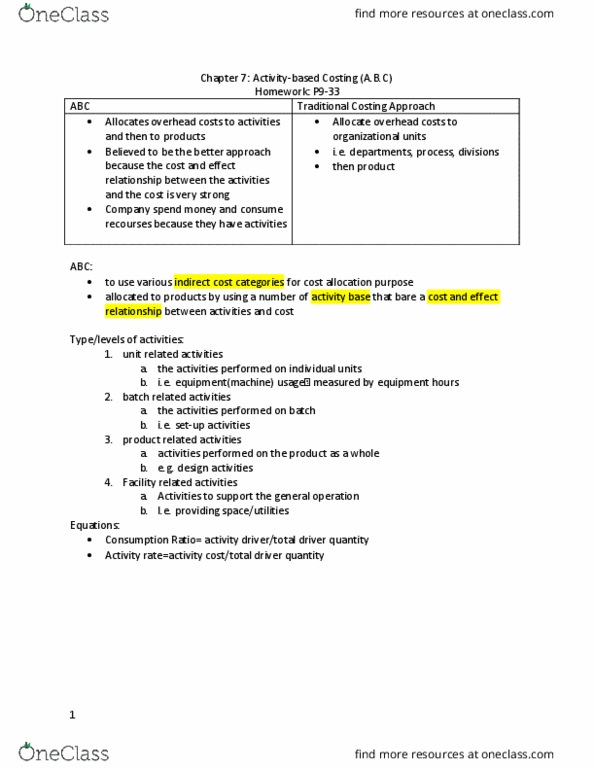

Tommy Lyons Company manufactures and sells two products: Product S3 and Product S2. Data concerning the expected production of each product and the expected total direct labor-hours (DLHs) required to produce the output appear below:

Product Info

Product S3: 800 units @ 8.0 DLH/unit = 6,400 hours

Product K2: 900 units @6.0 DLH/unit = 5,400 hours

Direct Material Cost/Unit

The direct labor rate is $18.00 per DLH. The direct materials cost per unit for each product is given below:

Product S3: $280.70

Product K2: $157.90

Activity Cost Pools

The company is considering adopting an activity-based costing system with the following activity cost pools, activity measures, total overhead costs and expected activity for each product.

Labor Related

Direct labor hours, total OH $523,094

S3 = 6,400

K2 = 5,400

Total = 11,800 DLHs

Machine Set-ups

Number of tests, total OH = $135,478

S3 = 600

K2 = 800

Total = 1,400 Tests

General Factory

Machine hours, total OH = $392,327

S3 = 5,000

K2 = 5,300

Total = 10,300 MHs

Total Overhead Costs

Including: DLHs, machine set-ups, machine hours = $1,050,899

Required:

The company currently uses a traditional costing methodin which overhead is applied to products based solely on direct labor-hours. Compute the company's predetermined overhead rate under this costing method.

How much overhead would be applied to each product under the company's traditional costing method?

Determine the unit product cost of each product under the company's traditional costing method.

Compute the activity rates under the activity-based costing system.

Determine how much overhead would be assigned to each product under the activity-based costing system.

Determine the unit product cost of each product under the activity-based costing method.

What is the difference between the overhead per unit under the traditional costing method and the activity-based costing system for each of the two products?