ACC 406 Lecture Notes - Lecture 4: Operating Leverage, Earnings Before Interest And Taxes, Fixed Cost

14 Oct 2017

School

Department

Course

Professor

Document Summary

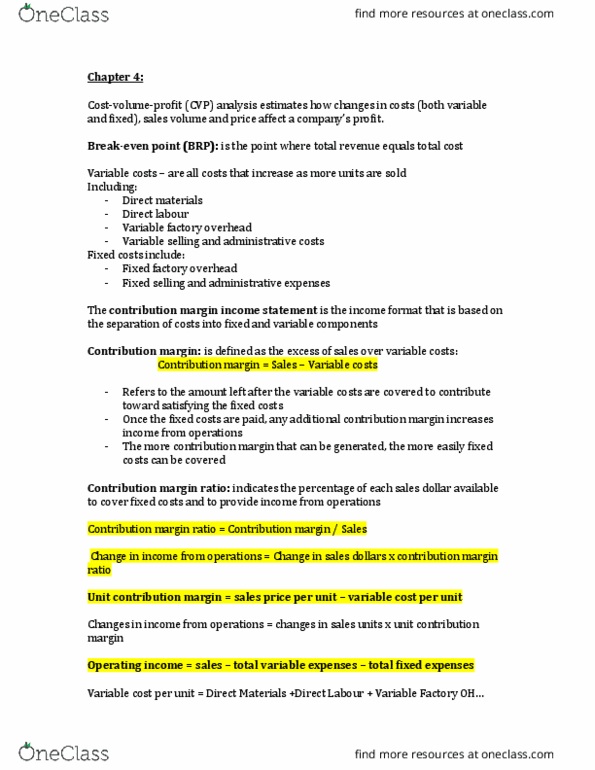

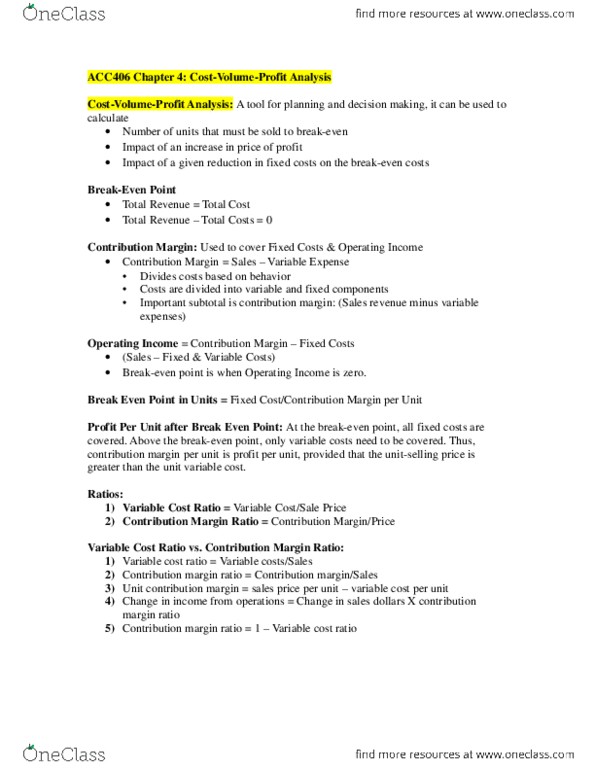

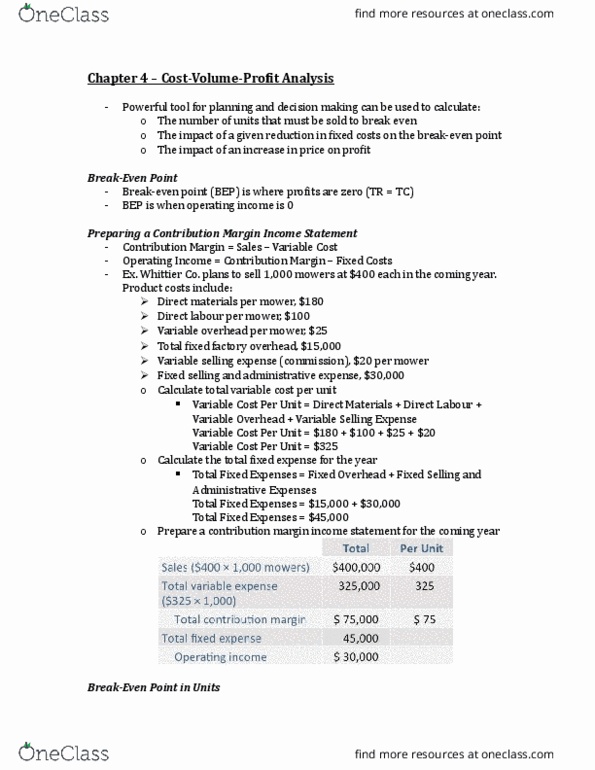

Sales variable cost = contribution margin. Contribution margin fixed costs = operating income. Operating income = sales total variable expenses total fixed expenses. Break-even number of units = total fixed expenses/ price variable cost. Units to be sold to achieve a target income. # (cid:1873)(cid:1866)(cid:1872)(cid:1871) (cid:1872)(cid:1867) (cid:1857)(cid:1853)(cid:1870)(cid:1866) (cid:1872)(cid:1853)(cid:1870)(cid:1859)(cid:1857)(cid:1872) (cid:1866)(cid:1855)(cid:1867)(cid:1865)(cid:1857)= (cid:1868)(cid:1870)(cid:1855)(cid:1857) (cid:1874)(cid:1853)(cid:1870)(cid:1853)(cid:1854)(cid:1864)(cid:1857) (cid:1855)(cid:1867)(cid:1871)(cid:1872) (cid:1868)(cid:1857)(cid:1870) (cid:1873)(cid:1866)(cid:1872) (cid:4666)(cid:4667) (cid:1871)(cid:1853)(cid:1864)(cid:1857)(cid:1871) (cid:1856)(cid:1867)(cid:1864)(cid:1864)(cid:1853)(cid:1870)(cid:1871) (cid:1872)(cid:1867) (cid:1857)(cid:1853)(cid:1870)(cid:1866) (cid:1872)(cid:1853)(cid:1870)(cid:1859)(cid:1857)(cid:1872) (cid:1866)(cid:1855)(cid:1867)(cid:1865)(cid:1857)= (cid:1858)(cid:1857)(cid:1856) (cid:1855)(cid:1867)(cid:1871)(cid:1872)+(cid:1872)(cid:1853)(cid:1870)(cid:1859)(cid:1857)(cid:1872) (cid:1866)(cid:1855)(cid:1867)(cid:1865)(cid:1857) (cid:1870)(cid:1853)(cid:1872)(cid:1867) Visually portrays the relationship between profits and units sold. The profit-volume graph is the graph of the operating income equation. Depicts the relationship among cost, volume and profit. Graphs two separate lines: total revenue; total cost. Assumptions: revenue and cost functions are linear, all units produced are sold, sales mix is constant, selling prices and costs are known with certainty. Sales mix is difficult to predict with certainty. Assumes cost and revenue functions are linear.