BU397 Lecture Notes - Lecture 4: Special Purpose Entity, Operating Lease, Conceptual Framework

Document Summary

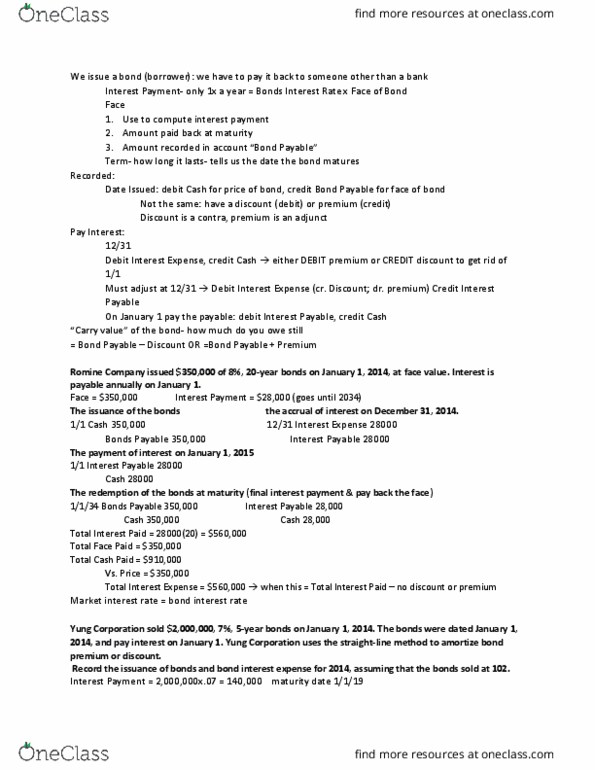

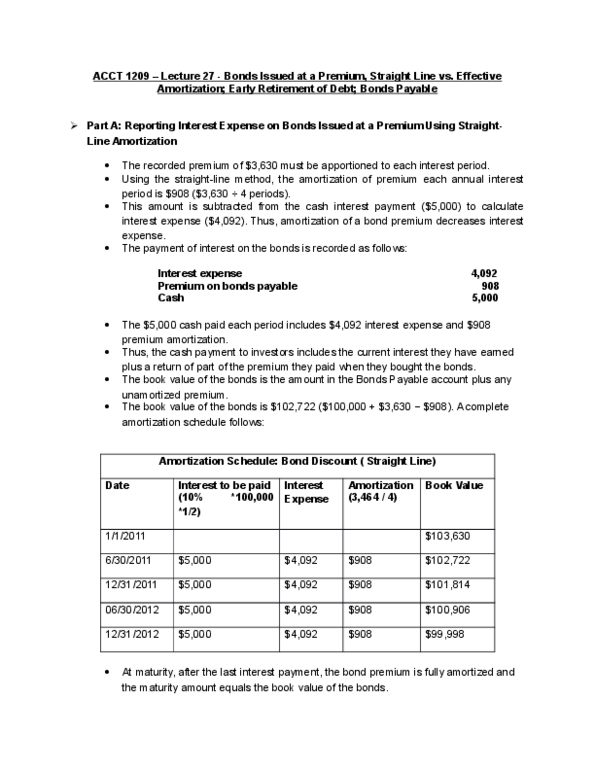

Bond maturity = 10 years: the annual discount amortization = ,000/10 years = ,400, the entry to record the annual discount amortization would be: 80,000: straight-line method premium, given, face value = ,000, stated rate = 10% Bond maturity = 10 years: the annual premium amortization =,000/10 years = ,400, the entry to record the annual premium amortization would be. Cash: the journal entry to record the bond issuance is: Cash: the journal entry for first semi-annual payment is: If the issued debt is a marketable security, the value of the transaction would be equal to fair value of the marketable security. Ifrs requires the fair value option only if it results in more relevant information. Includes any call premium and expenses: at the time of reacquisition all outstanding premiums, discounts, and issue costs are amortized to the date of reacquisition.