MGCR 211 Chapter Notes - Chapter 8: Capital Cost Allowance, Capital Asset, Intangible Asset

18 Feb 2013

School

Department

Course

Professor

Document Summary

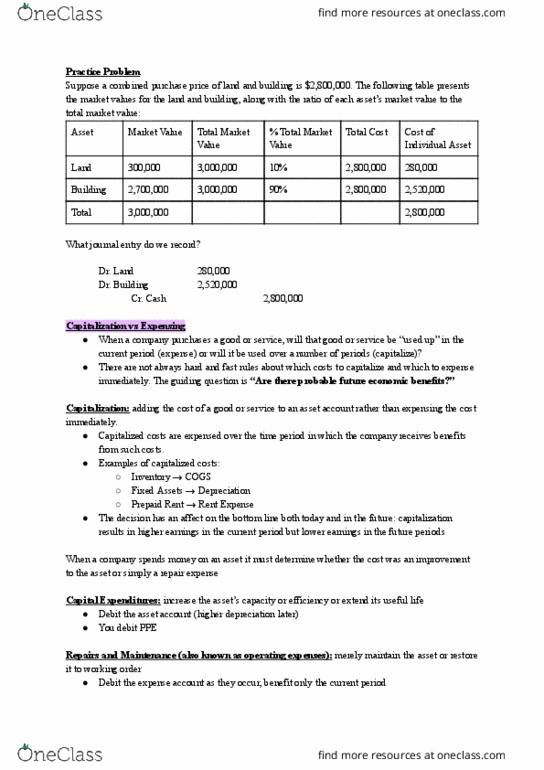

Capital asset: assets with lives longer than a year that are used in the company"s operations to generate revenue. Probable future value of an asset capital assets are used to generate revenues, usually by producing products, facilitating sales, or providing services. Ultimate disposal value use for some years then replace them/ sell them . etc. -- residual value the asset"s expected value at the end of its use. Asset"s original cost is recorded at the time of acquisition. Changes in the asset"s market value are ignored in this system. ***** during the period in which the asset is used, its cost is expensed (depreciated) using an appropriate depreciation method. Market values are recognized only when the asset is sold. Replacement cost : the amount that would be needed to acquire an equivalent asset. Net realizable value: assets are recorded at the amount that could be received by converting them cash (ie selling them)