ACC 406 Chapter 11: acc406 Chap11

18 Apr 2018

School

Department

Course

Professor

Document Summary

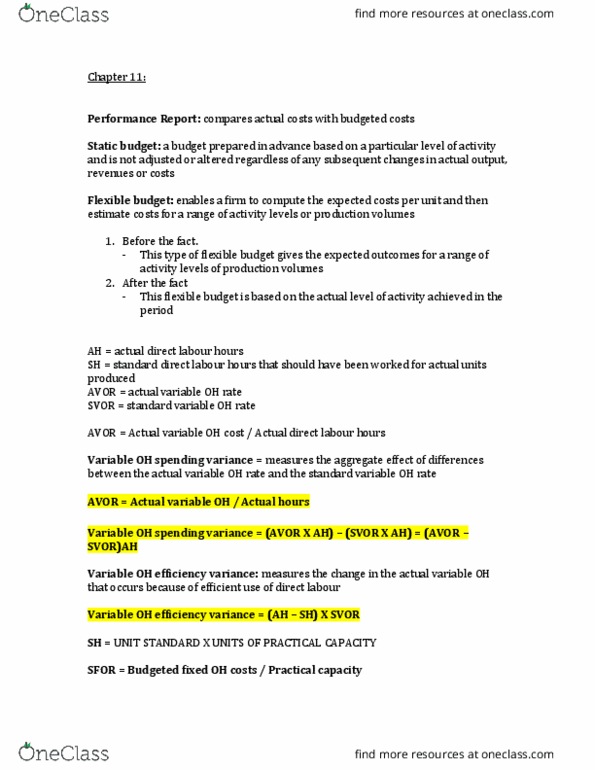

Chapter 11: flexible budgets & overhead analysis: performance reporting. Performance reports: compare actual costs with budgeted costs. Two ways: based on a static budget: compare actual costs with budgeted costs for the budgeted level of activity, based on a flexible budget: compare actual costs with the actual level of activity. Static budget: a budget for one particular level of activity. Direct materials, direct labor, and overhead costs budgeted for the planned level of activity with. Actual costs for the actual level of activity: to create a meaningful performance report: Actual costs and expected costs must be compared at the same level of activity. Expected costs are then compared with the actual costs in order to assess performance. For the flexible budget you compare a range of activities (ex: 1000 units, 1200 units, Then you compare the actual activity level with the budget.