ACC 410 Chapter Notes - Chapter 3: Contribution Margin, Variable Cost, Operating Leverage

14 May 2011

School

Department

Course

Professor

Document Summary

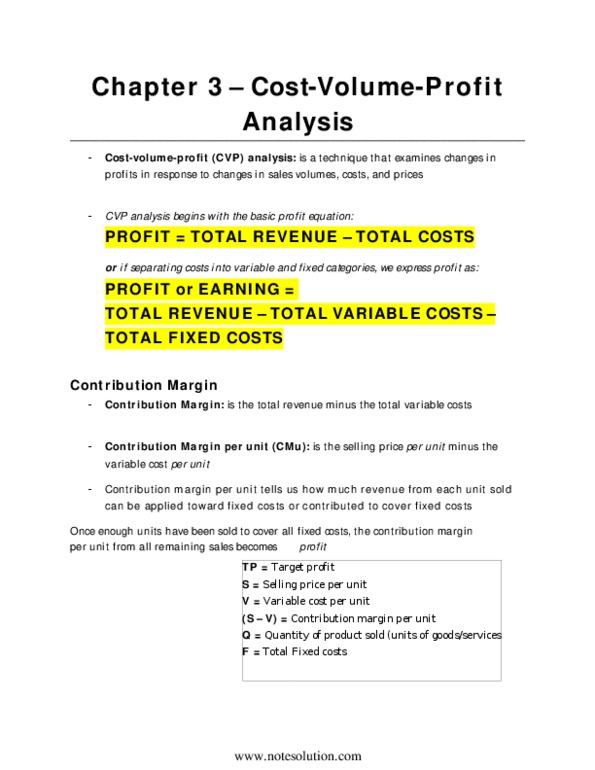

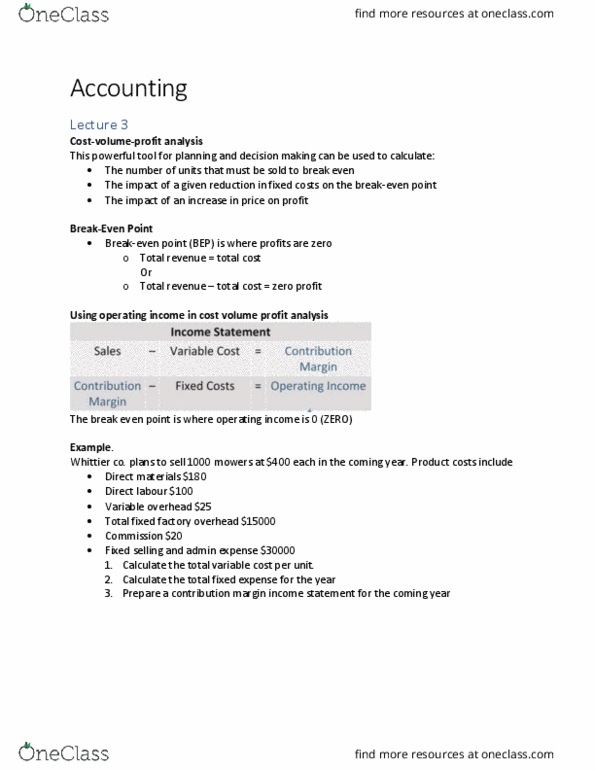

Various concepts will be covered such as the unit contribution margin, the break-even point, the cm ratio, margin of safety, operating leverage, and the sales mix: the basics of cost-volume-profit (cvp) analysis. Cost-volume-profit (cvp) analysis is a key step in many decisions. Cvp analysis involves specifying a model of the relations among the prices of products, the volume or level of activity, the unit variable costs, the total fixed costs, and the mix of products sold. This model is used to predict the impact on profits of changes in those parameters: contribution margin. Contribution margin is the amount remaining from sales revenue after variable expenses have been deducted. It contributes towards covering fixed costs and then towards profit: unit contribution margin. When there is a single product, the unit contribution margin can be used to predict changes in the contribution margin and in profits (assuming there is no change in fixed costs) as a result of changes in unit sales.