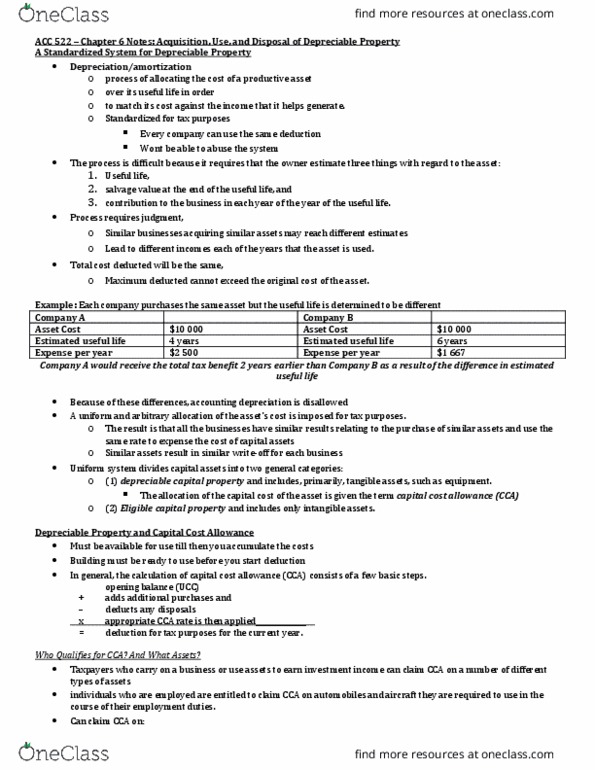

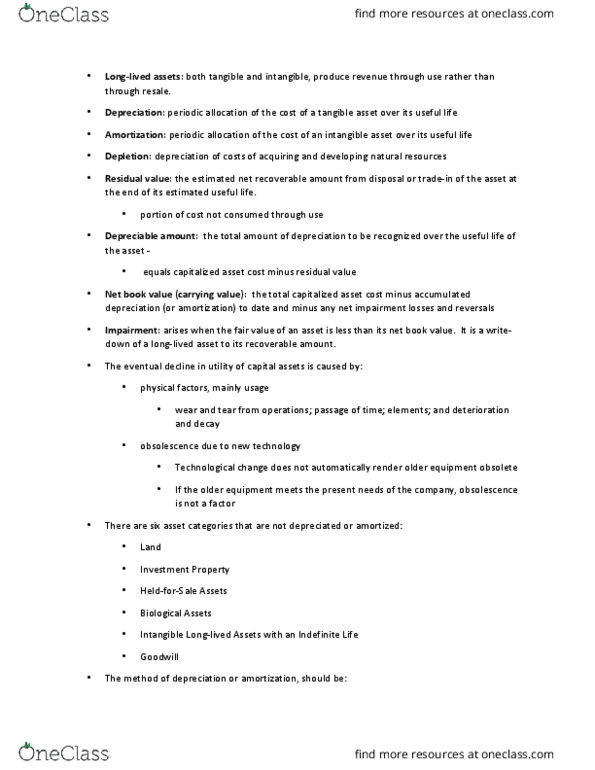

ACC 522 Chapter Notes - Chapter 6: Capital Cost Allowance, Capital Asset, Intangible Property

Document Summary

Get access

Related Documents

Related Questions

You have obtained the following information:

STATEMENT OF COMPREHENSIVE INCOME FOR THE YEAR TO 31 DECEMBER

| 20X8 | 20X7 | |||

| Note | Draft ($m) | Actual ($m) | ||

| Revenue | (1) | 645.5 | 606.5 | |

| Other income | (2) | 15.6 | 14.4 | |

| Changes in inventories | 3.8 | (16.4) | ||

| Cost of materials | (334.1) | (286.8) | ||

| Employee benefits expense | (91.0) | (83.9) | ||

| Depreciation | (3) | (29.8) | (23.6) | |

| Other expenses | (4) | (116.3) | (100.6) | |

| Interest income, net | (5) | 12.3 | (20.9) | |

| Profit before tax | 106.0 | 130.5 | ||

| Income tax expense | (44.4) | (47.7) | ||

| Profit for the year | 61.6 | 82.8 |

STATEMENT OF FINANCIAL POSITION AT 31 DECEMBER

| 20X8 | 20X7 | |||

| Note | Draft ($m) | Actual ($m) | ||

| Assets | ||||

| Non-current assets | ||||

| Intangible assets | (6) | 47.8 | 40.5 | |

| Property, plant and equipment | (7) | 124.5 | 102.5 | |

| 172.3 | 143.0 | |||

| Current assets | ||||

| Inventories | (8) | 30.3 | 27.9 | |

| Trade receivables | 73.1 | 50.3 | ||

| Cash and cash equivalents | 111.4 | 86.0 | ||

| Total assets | 387.1 | 307.2 | ||

| Equity and liabilities | ||||

| Equity | 5.8 | 5.8 | ||

| Share capital | 15.3 | 15.3 | ||

| Share premium | 112.1 | 80.1 | ||

| Retained earnings | 133.2 | 101.2 | ||

| Non-current liabilities | ||||

| Provisions | (9) | 160.1 | 121.4 | |

| Current liabilities | ||||

| Trade payables | 33.5 | 31.8 | ||

| Tax | 50.4 | 44.3 | ||

| Other liabilities | 9.9 | 8.5 | ||

| Total equity and liabilities | 387.1 | 307.2 |

Notes

(1) Revenue from business activities:

| Revenue from business activities | ||

| 20X8 ($M) | 20X7 ($M) | |

| Vehicles | 588.0 | 526.0 |

| Parts and accessories | 39.6 | 36.8 |

| Other | 17.9 | 43.7 |

| 645.5 | 606.5 | |

Other income includes gains on the disposals of tangible assets and income from the reversal of provisions.

Average number of employees:

| 20X8 (Draft) | 20X7 (Actual) | |

| Wage earners | 484 | 499 |

| Salaried employees | 483 | 477 |

| Apprentices and trainees | 36 | 37 |

| 1,003 | 1,013 | |

Other expenses include costs for warranties, administration and distribution, maintenance and insurance.

Interest income, net:

| 20X8 (Draft ($m) | 20X7 (Actual $m) | |

| Interest and similar income | 16.8 | 25.1 |

| Interest and similar expenses | (4.5) | (4.2) |

| 12.3 | 20.9 |

Intangible assets include development costs, also franchises and industrial rights and licenses. During the year, $12.7 million (20X7 - $6.3 million) was spent on developing a new sports model, the Fox.

Property, plant and equipment:

| Land and Buildings | Equipment | Assets under construction | Total | |

| $m | $m | $m | $m | |

| Cost | ||||

| 1 January 20X8 | 61.8 | 212.1 | 19.0 | 292.9 |

| Additions | 5.0 | 28.9 | 9.4 | 43.3 |

| Disposals | 0.0 | (4.5) | 0.0 | (4.5) |

| Reclassification | 3.0 | 8.9 | (11.9) | 0.0 |

| 31 December 20X8 | 69.8 | 245.4 | 16.5 | 331.7 |

| Depreciation | ||||

| Current year | 1.9 | 18.4 | 0.0 | 20.3 |

| Accumulated | 28.7 | 178.5 | 0.0 | 207.2 |

| Net book value | ||||

| 31 December 20X8 | 41.1 | 66.9 | 16.5 | 124.5 |

| 31 December 20X7 | 34.9 | 48.6 | 19.0 | 102.5 |

(8) Inventories comprise:

| 20X8 (Draft $m) | 20X7 (Draft $m) | |

| Raw materials, consumables and supplies | 8.3 | 7.3 |

| Work-in-progress | 6.8 | 4.8 |

| Finished goods | 15.2 | 15.8 |

| 30.3 | 27.9 | |

(9) Provisions mainly cover manufacturing warranty, product liability and litigation risks. Also, provisions have been established for deferred maintenance and IT reorganization.

The following additional information is available:

(i) Pavia has achieved record sales in 20X8 with the delivery of 10,153 vehicles (20X7 â 7,642 vehicles).

(ii) Although some sales are direct to individual customers the majority are ordered through dealers who take new vehicles on consignment.

(iii) Since 1 January 20X8 Pavia has offered 0% finance for three years on new vehicle sales in its most competitive markets.

(iv) The launch of the Fox has been postponed from late 20X8 to early 20X9 as internal trials have revealed that the doors are not sufficiently secure at high speeds.

(v) A car part required for the Cipeta model is bought-in exclusively from an overseas manufacturer. Deliveries of supplies have been unpredictable in 20X7 causing disruption to the Cipeta model assembly schedules.

1. Evaluate how you might use analytical procedures to provide audit evidence and reduce the level of detailed substantive procedures.

N.B these are pointers are for this question:

Analytical Procedures - Examples: o Receivables - Receivables - Compare gross margin % with previous years (by product line). (Possible misstatement â Over/understatement of sales and accounts receivable). This analytics will reduce the detailed substantive procedure because we have identified that there may be a possible over/understatement of sales so now we need to perform additional audit procedures on sales/revenue. For example by selecting a sample of invoices generated throughout the year and comparing to the General Ledger to ensure completeness and accuracy. Note: Use the information in the case to calculate the analytical procedures you have identified. Also, explain how the analytical procedures will provide audit evidence and help to reduce the level of detailed substantive procedures.