FIN 501 Chapter Notes - Chapter 7: Dividend Discount Model, Retained Earnings, Cash Flow

17 Jul 2012

School

Department

Course

Professor

Document Summary

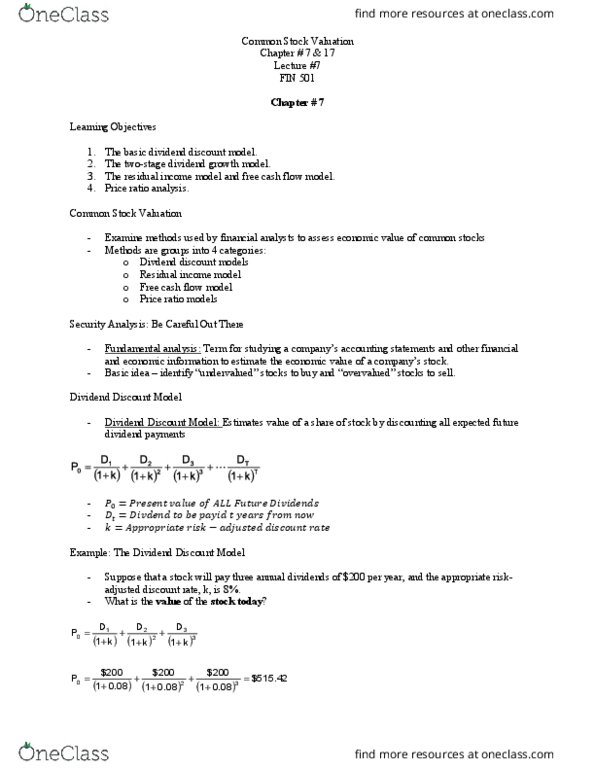

Fundamental analysis: examination of a firm"s accounting statements and other financial and economic information to assess the economic value of a company"s stock. Numbers such as a company"s earnings per share, cash flow, book equity value, and sales are often called fundamentals because they describe, on a basic level, a specific firm"s operations and profits (or lack of profits) A fundamental principle of finance holds that the economic value of a security is properly measured by the sum of its future cash flows, where the cash flows are adjusted for risk and the time value of money. Dividend discount model (ddm): method of estimating the value of a share of stock as the present value of all expected future dividend payments (where dividends are adjusted for risk and the time value of money) For example, suppose a company pays a dividend at the end of the year. Let d(t) denote a dividend to be paid t years from now.