FIN 501 Chapter Notes - Chapter 3: Canada Deposit Insurance Corporation, Web Browser, Td Waterhouse

17 Jul 2012

School

Department

Course

Professor

Document Summary

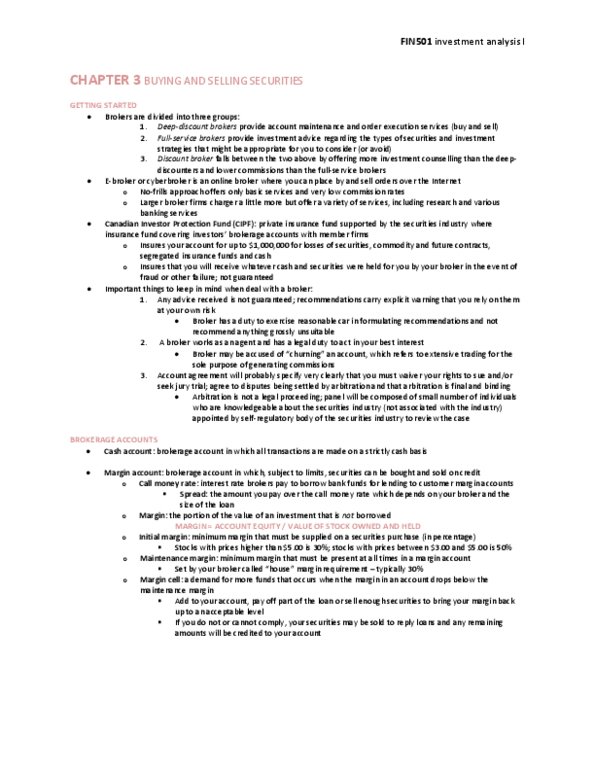

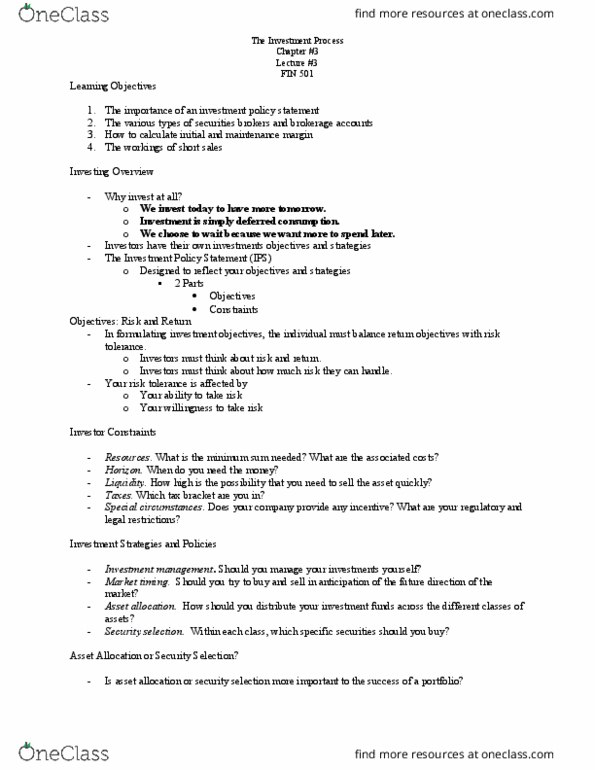

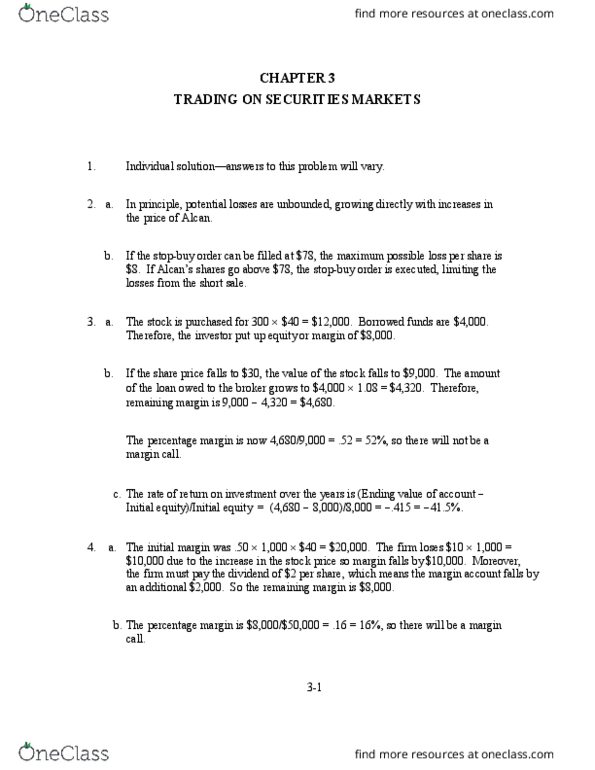

Brokerage or trading accounts: open an account with a securities broker, such as scotia mcleod or td. Waterhouse if you have some money that you want to invest. You will be asked to supply some basic information about yourself and sign an agreement (often called a customer"s agreement) that spells out your rights and obligations and those of your broker. You then give your broker a cheque and instructions on how you want the money invested. Ex: you open an account and instruct your broker to purchase shares of a company"s stock and to retain any remaining funds in your account. Your broker will locate a seller and purchase the stock on you behalf. In addition, for providing this service, your broker will charge you a commission. Your broker will hold your stock for you or deliver the shares to you, whichever you wish. At a later date, you can sell your stock by instructing your broker to do so.