FIN 701 Chapter Notes - Chapter 2: Credit Union, Payments Canada, Market Timing

18 Sep 2013

School

Department

Course

Professor

Document Summary

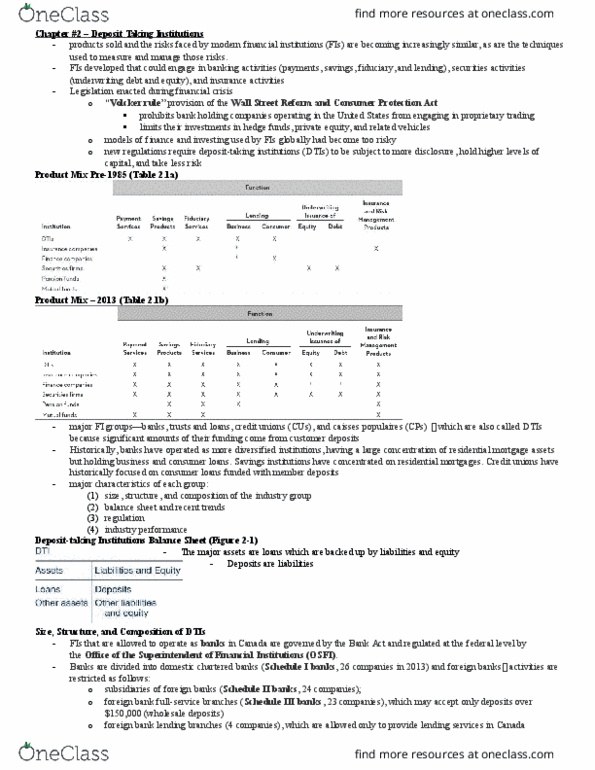

Banks, trusts and loans, credit unions, and caisses poplaires also called deposit-taking institutions (dtis) There are nine financial service powerhouses in canada called full-service fis, including the big six banks (bmo, bank of. Nova scotia, cibc, national bank of canada, rbc, and td) and the three largest insurance companies (manulife financial, Fis allowed to operate as banks in canada governed by the bank act and regulated at federal level by the office of the. Banks divided into domestic chartered banks (schedule i banks) and foreign banks whose activities are restricted: Foreign bank full-service branches (schedule iii banks) that may only accept deposits over ,000. Foreign bank lending branches that are only allowed to provide lending services in canada. Large canadian banks (equity > billion) must be widely held; no one person may hold more than 20% of voting shares.