ADMN 4710H Chapter Notes - Chapter 12: Capital Loss, Capital Gain, Deferral

30 Mar 2020

School

Department

Course

Professor

Document Summary

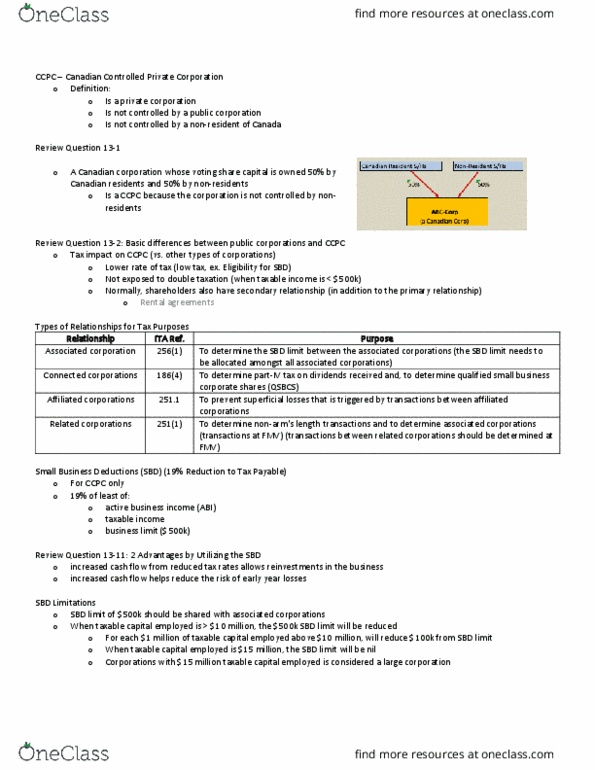

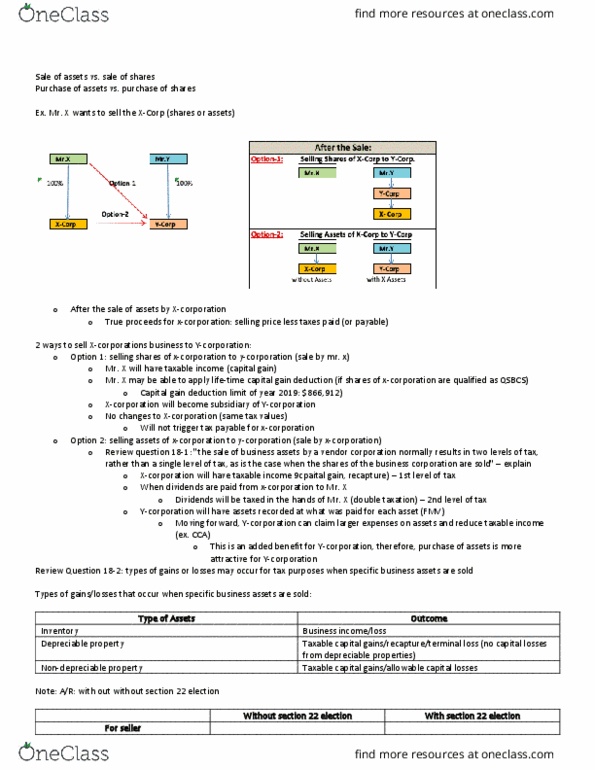

How to become a shareholder: acquire new shares from corporation, acquire previously issued shares from another shareholder. Example: year one shareholder (a) invests k in abc corp shares for shareholder: acb = k. For abc corp: puc = k, year 3. Shareholder (a) sells all shares to shareholder (b) for k. For shareholder (a: pod = k, acb = k, therefore, capital gain = k, taxable capital gain = k @ 50% For abc corp: puc = k, no tax impact to corporation. Abc corporation owned solely by shareholder mr. a has a value of ,000. Mr. b intends to acquire a 50% equity interest in the corporation. The cost to mr. b for acquiring 50% of the corporation"s shares may be either ,000 or ,000. Explain: option 1, mr. b can buy 50% of shares held by mr. a for ,000 and become a 50% owner of corporation.