RSM222H1 Chapter Notes - Chapter 7: Earnings Before Interest And Taxes, Fixed Cost, Variable Cost

Document Summary

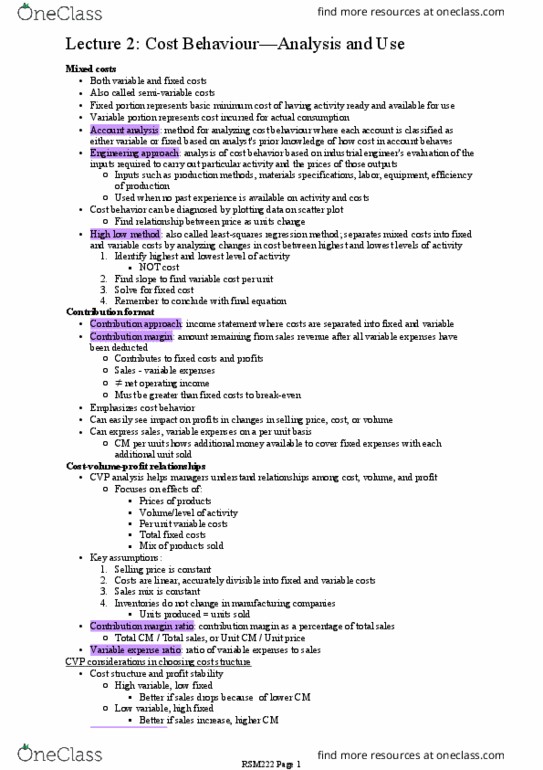

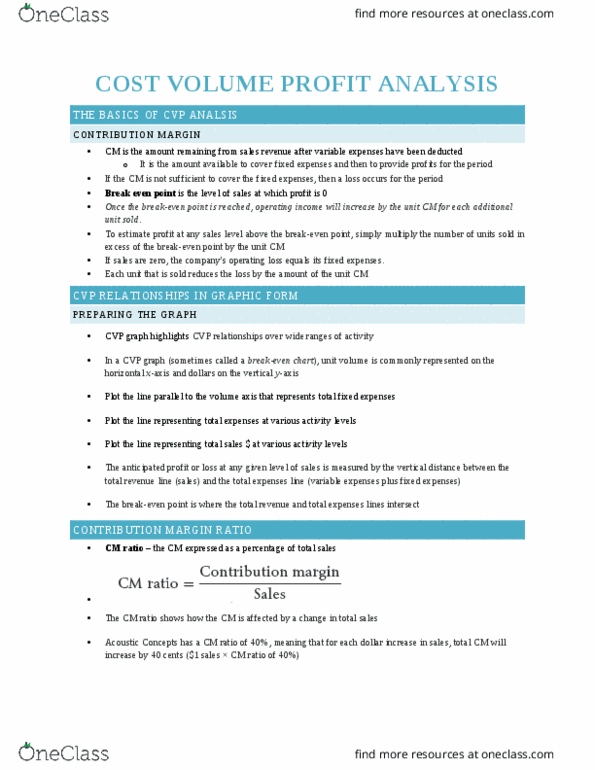

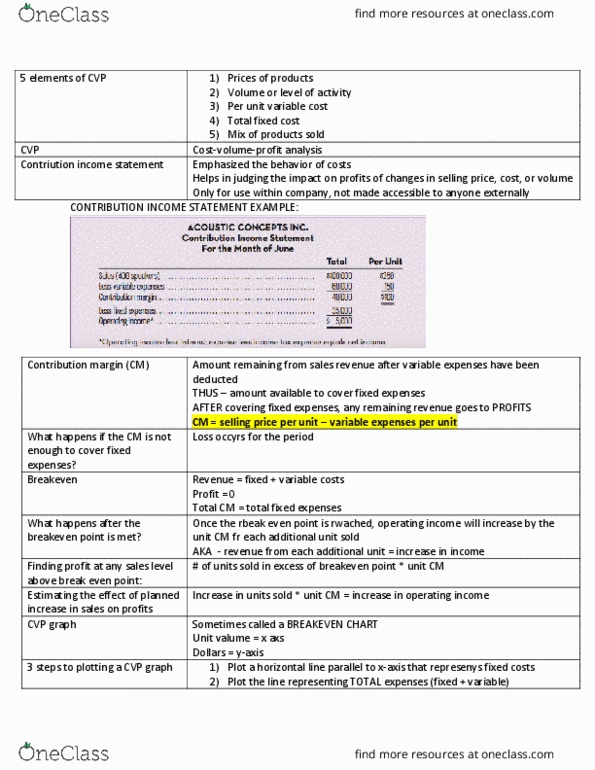

Cvp analysis is a powerful tool that helps managers to understand the relationships among cost, volume, and profit. It focuses on how profits are affected by the following 5 elements: prices of products, volume or level of activity, per unit variable costs, total fixed costs, mix of products sold. This is vital for decision making because this analysis helps managers understand how profits are affected by these factors ^ Reports sales, var expenses, and cm on both a per unit basis and a total basis. Use operating income as a measure of profit. If cm is not enough to cover the fixed exps, then a loss occurs for the period. For each additional x product that the company is able to sell, more in cm will become available to help cover the fixed exps. Fixed exps = sh: once this is reached, operating income will increase by the unit cm for each additional unit sold.