RSM222H1 Chapter Notes - Chapter 6: Total Absorption Costing, Indian Railways

Document Summary

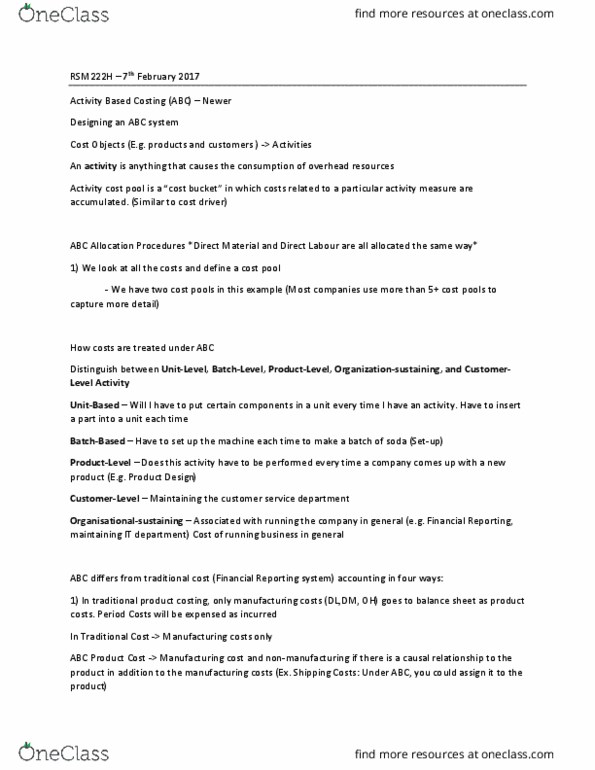

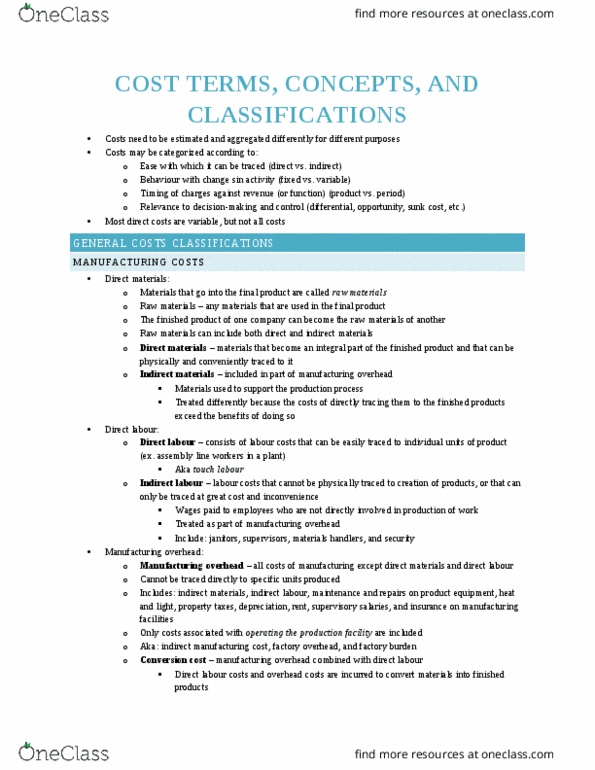

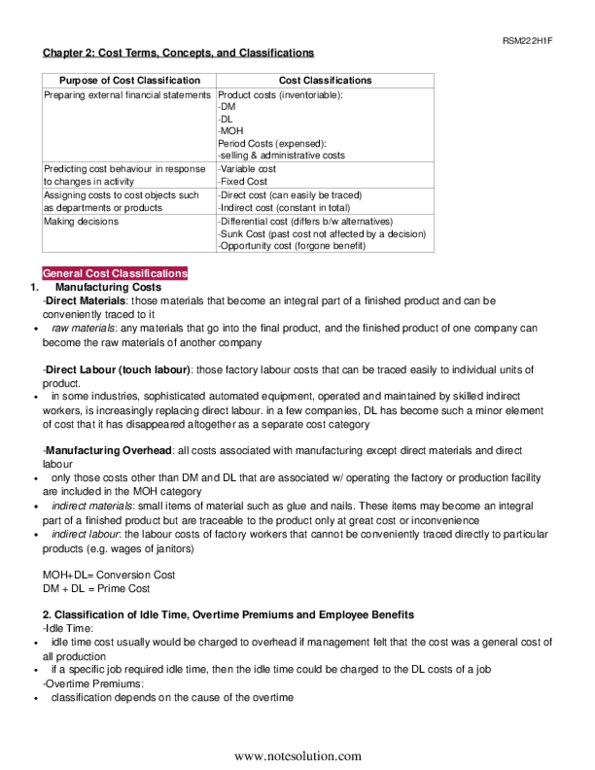

Week 4: systems design: process costing: process costing used for continuous production of homogenous product, form of absorption costing, accumulate costs by department. If production or costs fluctuate, then charging actual costs will result in unit costs varying randomly from period to period: should use predetermined rates if costs vary. Establish rate for each department: average cost is found by dividing total manufacturing cost by number of units produced. Production periods do not align with accounting units: use equivalent units. Equivalent units = number of partially completed units * % complete: fifo method: accounts for cost flows in process costing system where equivalent units and unit costs relate only to work done during current period. Weighted average: blends units and costs from current and prior periods: equivalent units of production (weighted-average method): units transferred to next department during period plus equivalent units in ending work in process inventory.