RSM222H1 Chapter Notes - Chapter 13: Payback Period, Capital Budgeting, Net Present Value

Document Summary

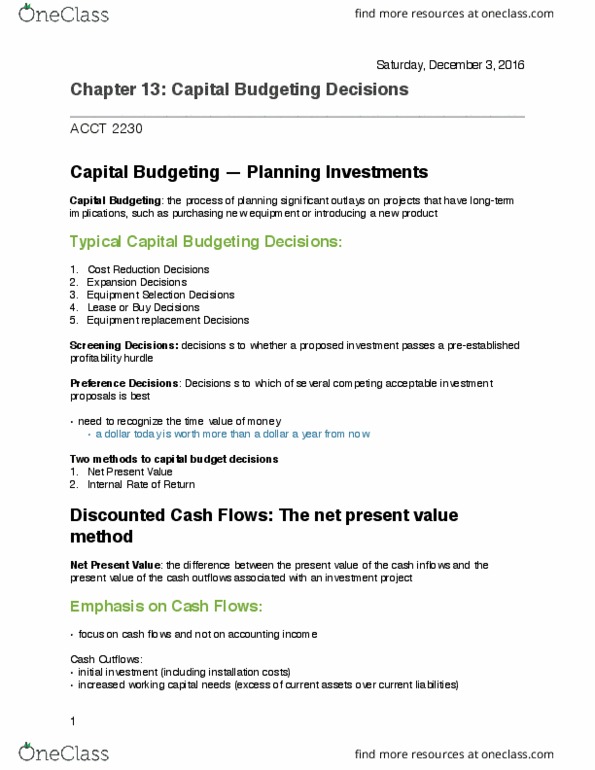

Week 11: chapter 13: capital budgeting decisions: capital budgeting: process of planning significant outlays on projects that have long-term implications. Types of capital budgeting decisions: cost reduction decisions. Cash flows of investment: typical outflows, typical inflows. Projects typically require firm to expand working capital. Periodic maintenance and repairs, incremental operating costs. Salvage value of equipment when project terminated. Released working capital at end of project. Preference decisions: can choose option with highest irr, can look at profitability index: pv of net cash inflows/investment required. Investment required include cash outflows at beginning net of any salvage value of old equipment and required investment in working capital: cannot base decision solely off irr if projects have different useful lives. A has life of one year, irr=20% B has life of six years, irr-16% While a has higher irr than b, b is preferable. Other methods: payback period = investment required / net annual cash inflow.