RSM324H1 Chapter Notes - Chapter 10: Pension Credit, Property Income, Dividend Tax

22 Feb 2017

School

Department

Course

Professor

Document Summary

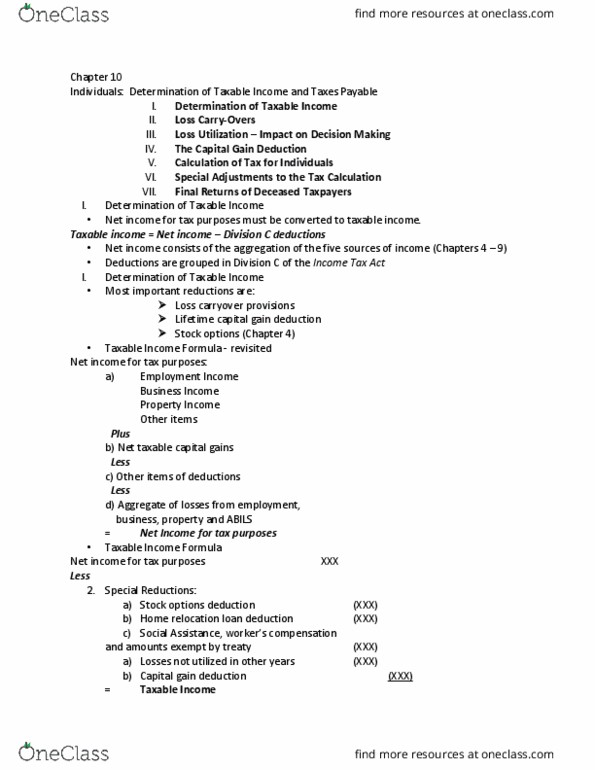

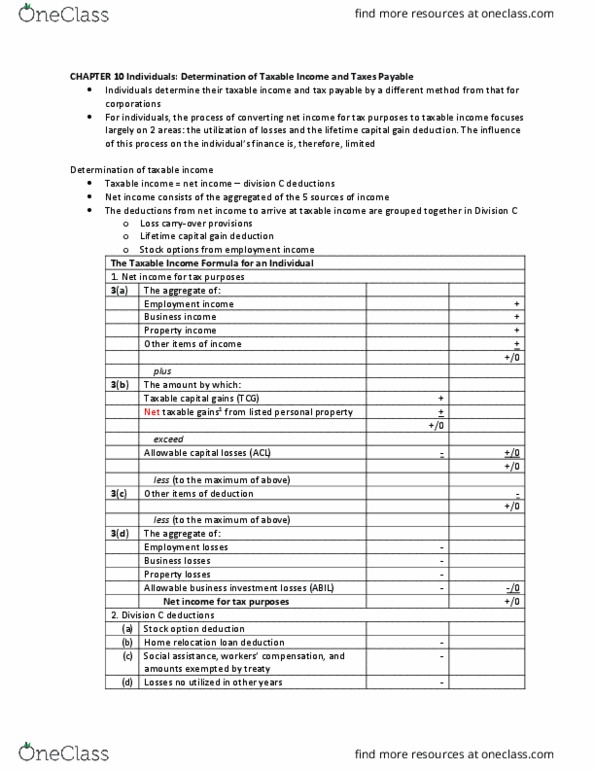

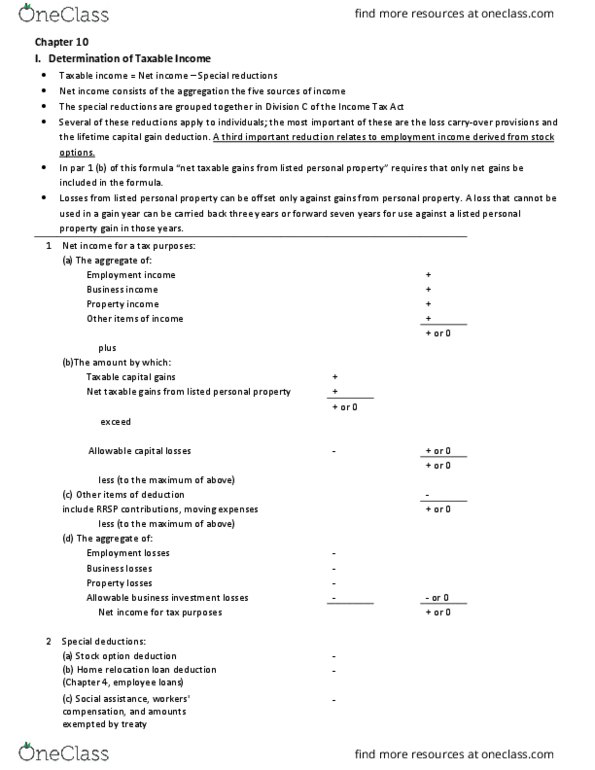

Chapter 10 individuals: determination of taxable income and taxes payable. The final step in arriving at the taxable income of an individual is to apply the capital gain deduction. The deduction applies only to gains realized on 3 specific types of property qualified small business corporation shares (qsbc), qualified farm property, and qualified property used in a family fishing business. The lifetime max deduction for qualified farm property and property used in a family fishing business is ,000,000 (,000 of net taxable capital gains) A qsbc must be a sbc at the time the shares are sold. The deduction is discretionary, and in some circumstances, it bay be desirable to forgo its use until a later year. The ability to claim the capital gain deduction is limited by 2 items capital losses incurred (including abil), and accumulated investment losses, which are referred to as the cumulative net investment loss (cnil)