RSM324H1 Chapter Notes - Chapter 10: Net Income, Property Income

22 Feb 2017

School

Department

Course

Professor

Document Summary

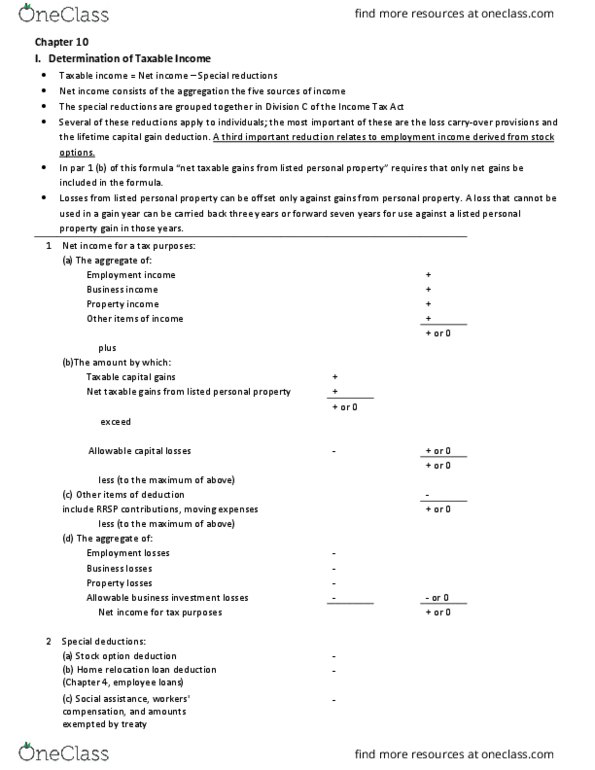

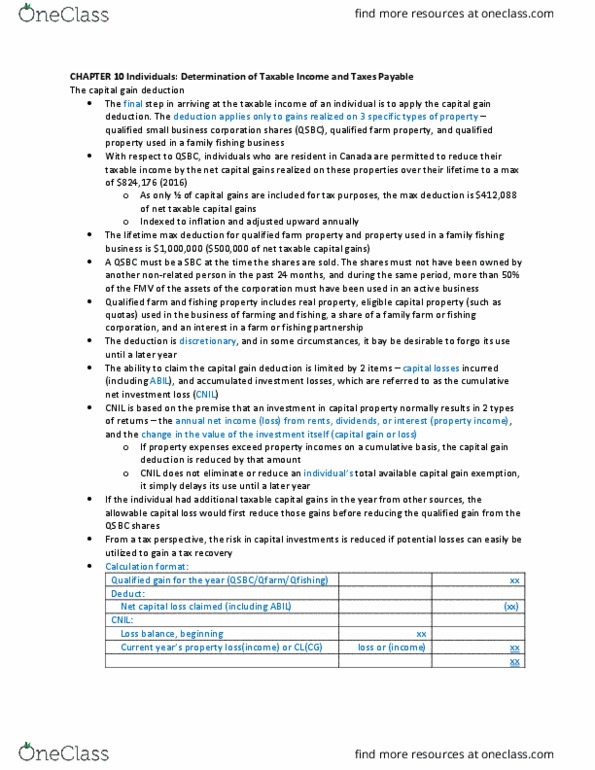

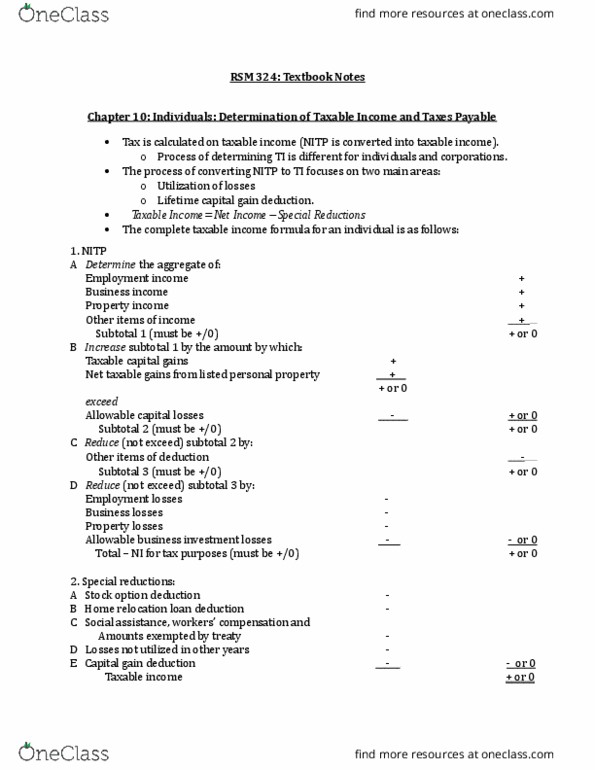

Chapter 10 individuals: determination of taxable income and taxes payable. Individuals determine their taxable income and tax payable by a different method from that for corporations. For individuals, the process of converting net income for tax purposes to taxable income focuses largely on 2 areas: the utilization of losses and the lifetime capital gain deduction. The influence of this process o(cid:374) the i(cid:374)di(cid:448)idual"s fi(cid:374)a(cid:374)ce is, therefore, li(cid:373)ited. Taxable income = net income division c deductions. Net income consists of the aggregated of the 5 sources of income. The deductions from net income to arrive at taxable income are grouped together in division c: loss carry-over provisions, lifetime capital gain deduction, stock options from employment income. The taxable income formula for an individual: net income for tax purposes. Net taxable gains1 from listed personal property exceed. Allowable capital losses (acl) less (to the maximum of above) Other items of deduction less (to the maximum of above)