RSM324H1 Chapter Notes - Chapter 10: Tax Rate, Tax Deduction, Tax Bracket

Document Summary

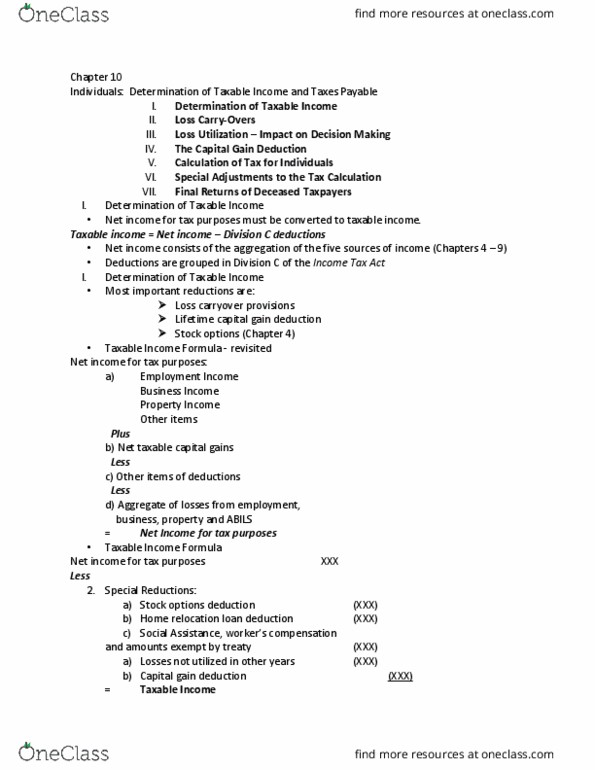

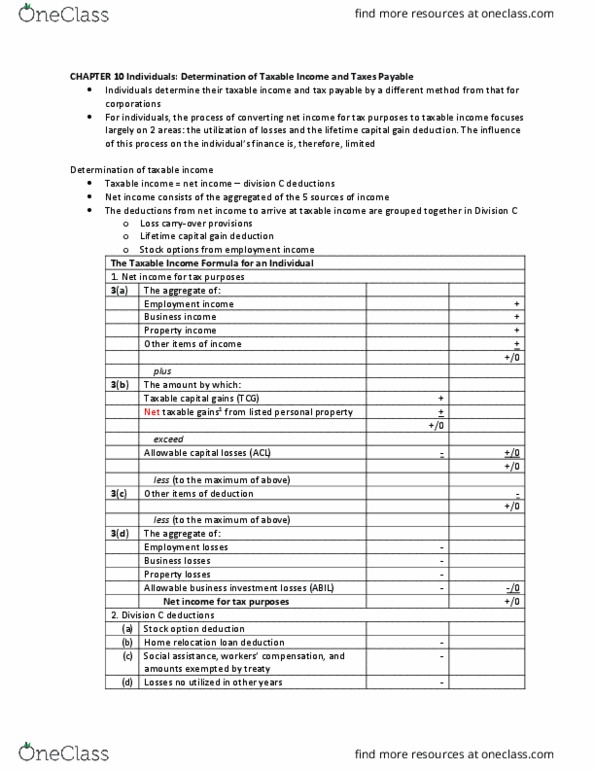

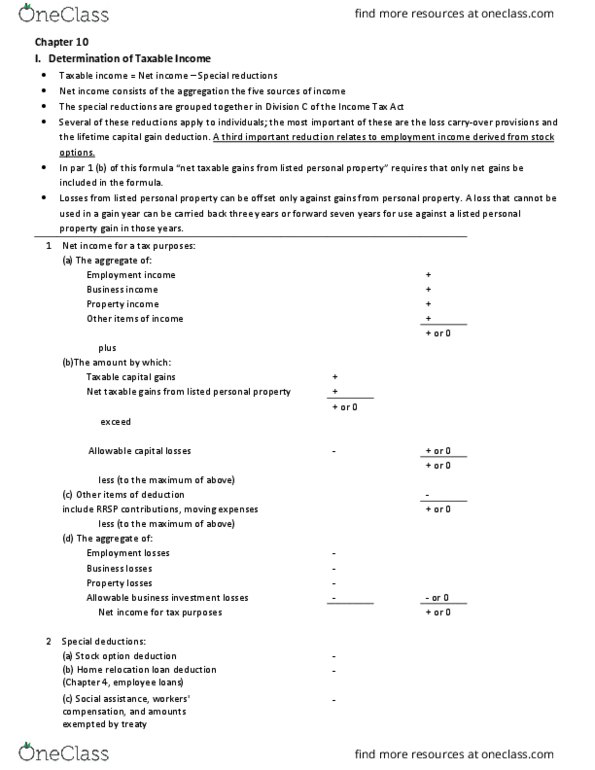

Chapter 10: individuals: determination of taxable income and taxes payable. Tax is calculated on taxable income (nitp is converted into taxable income): process of determining ti is different for individuals and corporations. The process of converting nitp to ti focuses on two main areas: utilization of losses, lifetime capital gain deduction. The complete taxable income formula for an individual is as follows: nitp. B increase subtotal 1 by the amount by which: Net taxable gains from listed personal property + Total ni for tax purposes (must be +/0) Special reductions cannot be merged with items in the nitp calculations since in some cases they depend on the amount of net income otherwise determined. The net income portion of the formula is reserved exclusively (except for lpp loss carry-overs) for transactions of the current year. The special reductions portion of the formula deals with transactions of other years or modifies the treatment of certain items in the net income portion.