BU247 Chapter Notes -Indirect Costs, Cost Driver, Management System

Document Summary

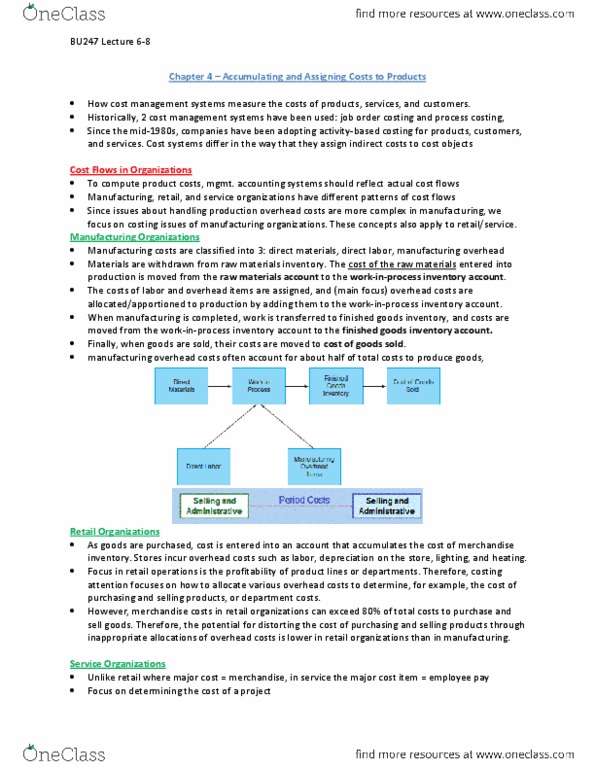

Chapter 4 accumulating and assigning costs to products. How cost management systems measure the costs of products, services, and customers. Historically, 2 cost management systems have been used: job order costing and process costing, Since the mid-1980s, companies have been adopting activity-based costing for products, customers, and services. Cost systems differ in the way that they assign indirect costs to cost objects. To compute product costs, mgmt. accounting systems should reflect actual cost flows. Manufacturing, retail, and service organizations have different patterns of cost flows. Since issues about handling production overhead costs are more complex in manufacturing, we focus on costing issues of manufacturing organizations. Manufacturing costs are classified into 3: direct materials, direct labor, manufacturing overhead. Materials are withdrawn from raw materials inventory. The cost of the raw materials entered into production is moved from the raw materials account to the work-in-process inventory account.