BU487 Chapter Notes - Chapter 4: Discounted Cash Flow, Business Valuation, Financial Statement

Document Summary

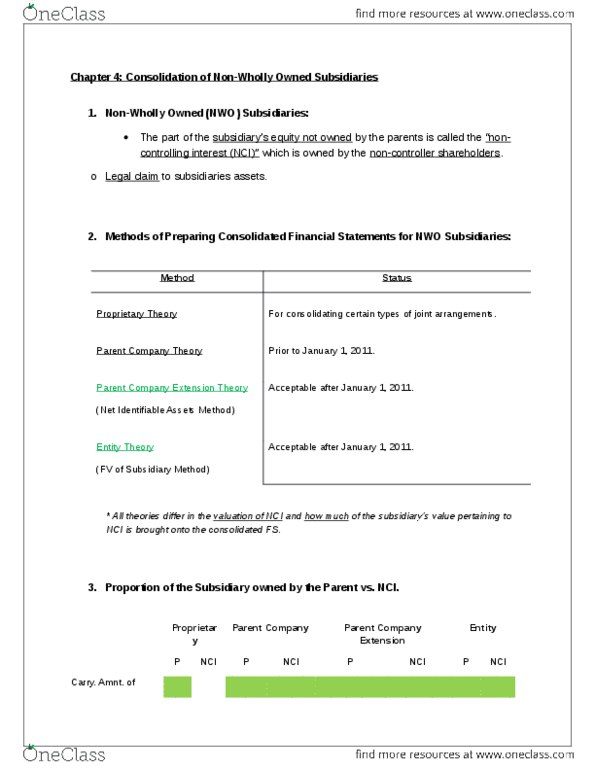

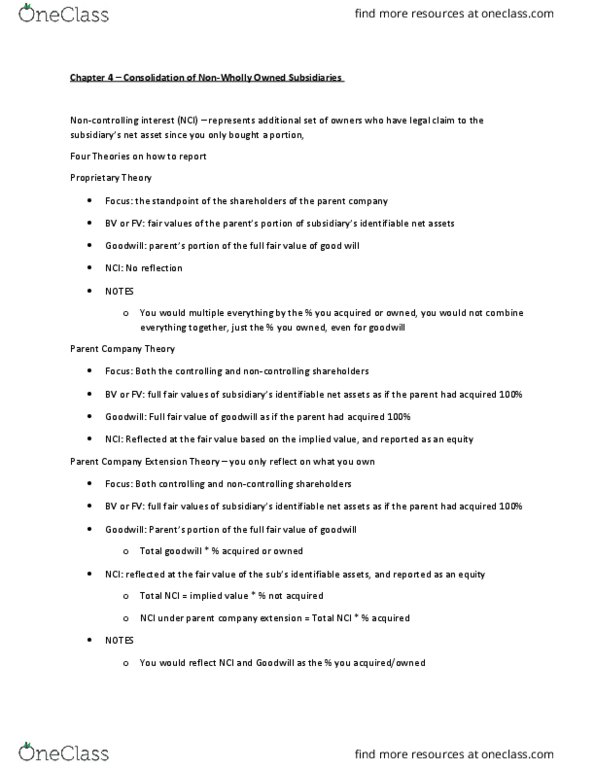

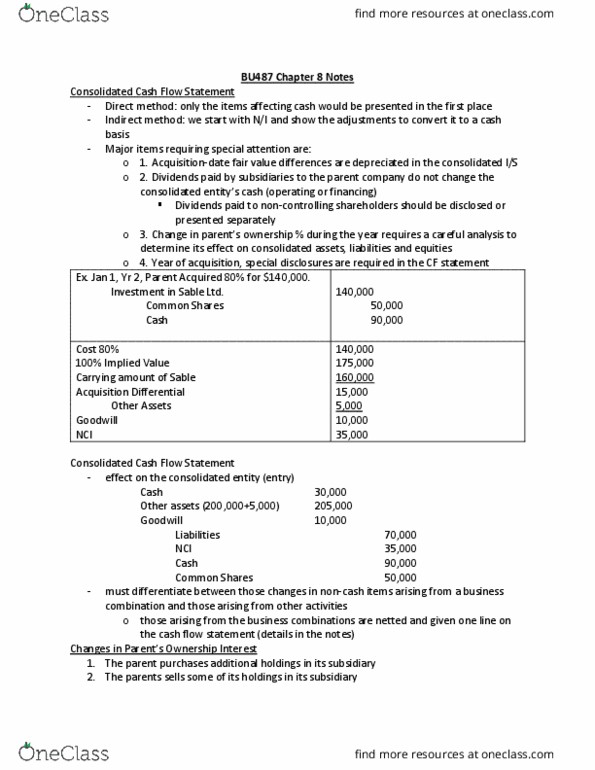

These balance sheets present the financial position just prior to the business combination. The part of the subsidiary not owned by the parent is called non-controlling interest (nci: non-controlling interest represents an additional set of owners who have legal claim to the subsidiary"s net assets. How should the portion of the subsidiary"s assets and liabilities that was not acquired by the parent be measured on the consolidated financial statements: 2. How should nci be measured on the consolidated financial statements: 3. Theories to prepare fs for non-wholly owned subsidiaries: proprietary theory, parent company theory (fair value of identifiable net assets or partial goodwill, parent company extension theory, entity theory. All four theories have ben or now are required under canadian gaap. June 20, yr 1, s ltd has 10,000 shares outstanding and p ltd. Purchases 8,000 shares (80%) of s ltd. for a total cost of ,000. P ltd. "s journal entry to record this purchase: investment in s ltd.