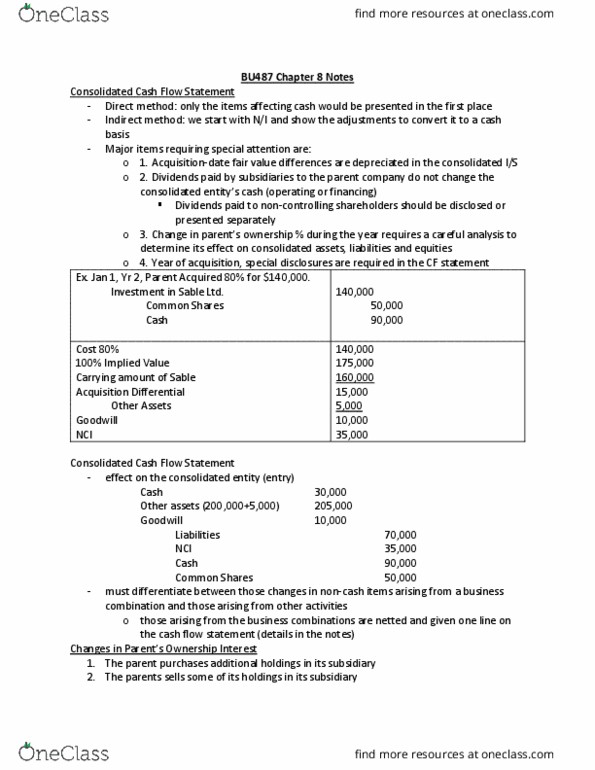

BU487 Chapter Notes - Chapter 8: Cash Flow Statement, Impaired Asset, Shares Outstanding

Document Summary

Chapter 8: consolidated cash flows and ownership issues: consolidated cash flow statement: Indirect method: start with ni and show adjustments to convert it to a cash basis: ex: Parent buys more holdings in the subsidiary (block acquisition). Parent sells some of its holdings in the subsidiary. Subsidiary issues c) maintain its previous ownership percentage. more common shares to the public; parent doesn"t d) Subsidiary repurchases some of its common shares from the nci. Note: if the parent"s share changes, the nci % changes. Note: when the parent"s ownership % increases/purchase (decreases/sale), a portion of the unamortized acquisition differential will be transferred from the nci (parent) to the parent (nci). 4. (a) block acquisitions of subsidiary (step purchases): the subsidiary is measured at fv on the date the parent obtains control, changes in reporting method are accounted for prospectively. Records the increase in the value of the associates share at reporting date.