ACTG 2011 Chapter Notes - Chapter 7: Cash Flow, Inventory Turnover, Accounts Payable

3 Oct 2014

School

Department

Course

Professor

Document Summary

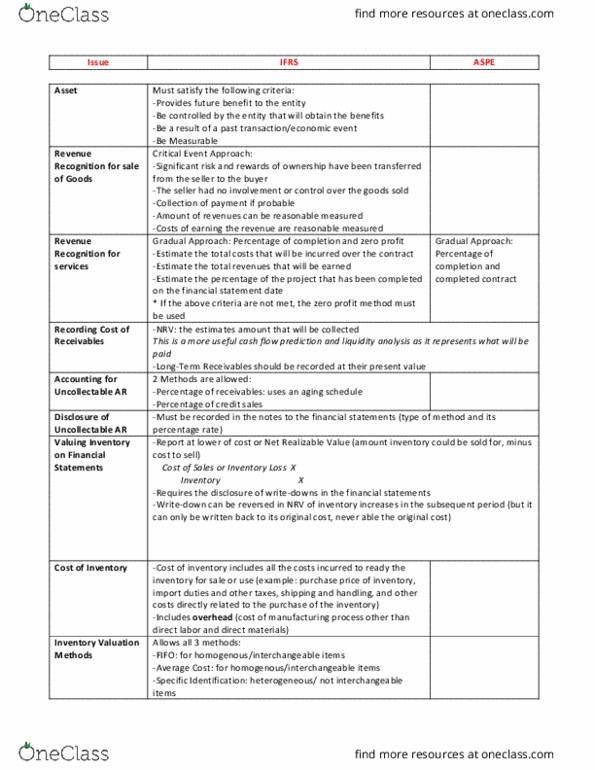

Essential to know value of inventory on hand and cost of inventory sold when we do not know the cost of the specific inventory sold/used. Inventory must be valued at cost on the balance sheet. Lowe of cost and nrv: if net realizable value is less than cost, inventory is written down to nrv. Must include all costs incurred to ready the inventory for sale/use; purchase price, import duties, taxes, shipping and handling, and other costs directly related to purchase of inventory. Must include cost of labour directly used to produce the product plus allocation of overhead. Overhead: costs in manufacturing process other than direct labour and materials. Following costs are to be excluded: storage, administration, selling and marketing, and waste. Goods on consignment reported in inventory of the manufacturer/distributor, and not in inventor of the seller (party that has possession of the inventory) Goods in transit included in inventory of the buyer if title has transferred.