ADMS 3520 Chapter Notes - Chapter 7: Capital Gains Tax, Unemployment Benefits, Tax Shelter

9 Aug 2012

School

Department

Course

Professor

Document Summary

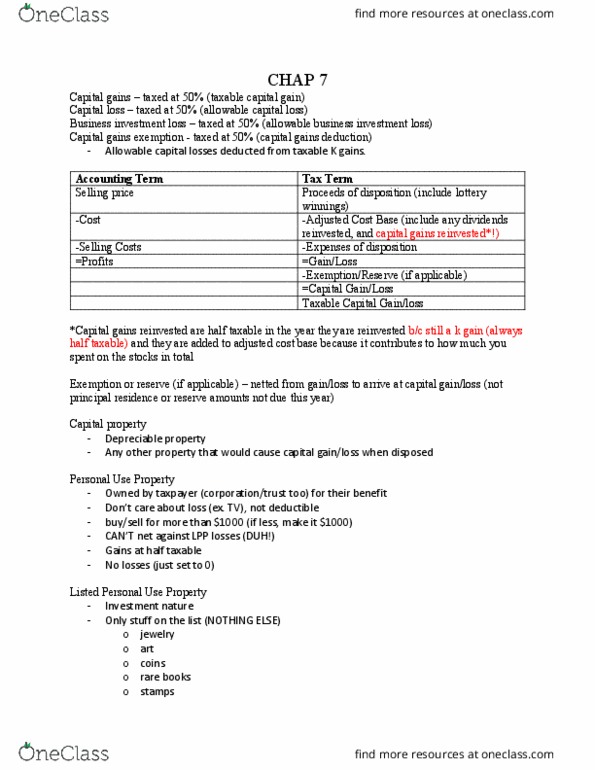

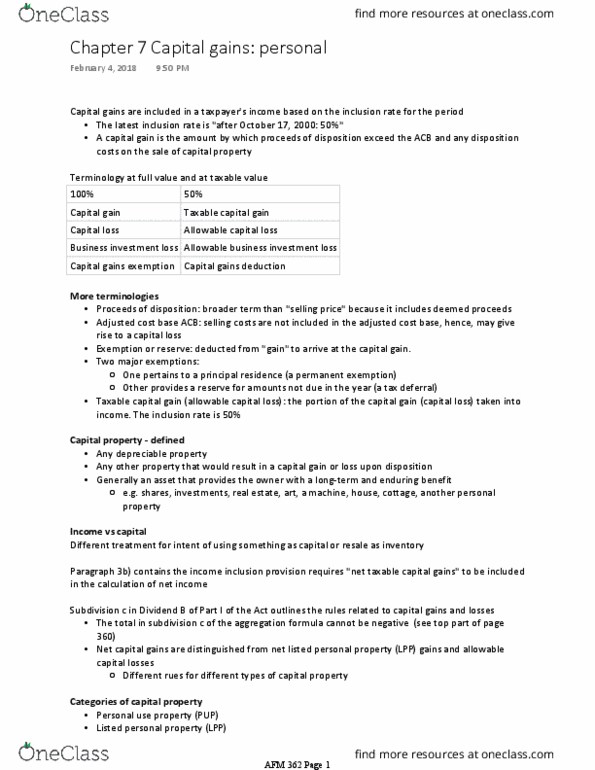

Defined as gains on disposal of capital property (assets) Capital assets are assets which are capable of earning income in the form of business profits, interest, dividends, rents or royalties. Taxable capital gain = 50% of capital gain. Allowable capital losses = 50% of capital loss these can be applied against taxable capital gains there was no capital gains tax before 1972. All assets owned at december 31, 1971 are valued at that date. This is called their v-day value. for the sale of assets owned at december 31, 1971, there are two methods to calculate the capital gain. These are the median rule and the v-day valuation method. Acb of the asset sold is the middle value between cost, v-day value and proceeds. Acb of asset sold is the v-day value of the asset. Identical properties :cost of shares disposed of is determined by the weighted average cost method as follows: 1000 x = 50,000 acb = 159,100.