COMMERCE 1AA3 Lecture Notes - Lecture 12: Cash Flow, Accrual, Net Income

17 Jun 2015

School

Department

Course

Professor

Document Summary

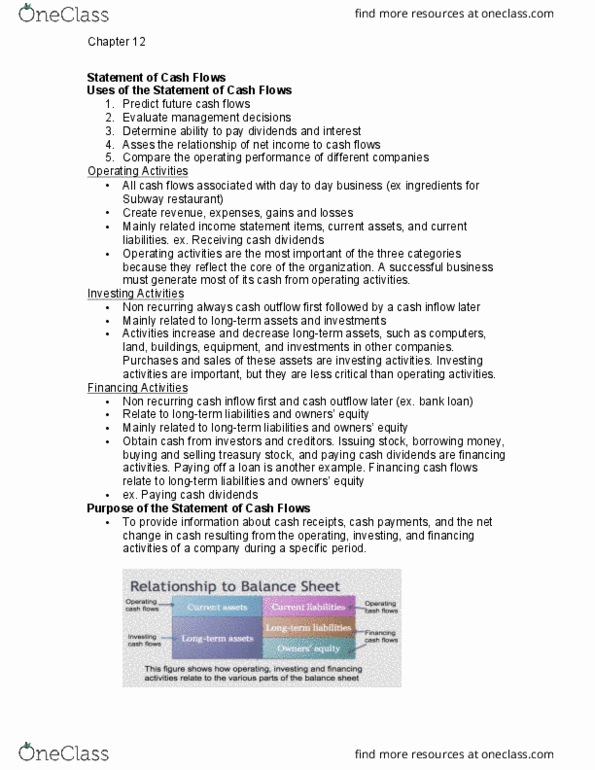

Chapter 12: cash flows: prepare cash flow statements to provide information about cash receipts, cash payments, net changes, etc, the income statement under the cash basis, provides predictive ability specifically operating activities. Unless part of a long-term plan- if you have a segment that is losing money, plan withdrawls from sections: financing activities deal with liabilities and equity. Investing activities: relate to long-term assets, financing activites, long-term liabilities, owner"s equity, preparing the statement of cash flows, doesn"t require a trial balance (unlike other statements) Income statement and balance sheet do require a trial balance: only statement not done under the accrual basis, requires: Comparative balance sheet (current and last year) Additional information: cash from operating activities. Most companies use the indirect method: reveals less company information to competitors. Direct method: cash flows from operating activities, collections from customers, payments to suppliers, payments for operating expenses, payments for income taxes, more informative, shows you how much you paid for everything.