MKT 300 Chapter Notes - Chapter 3: Contribution Margin, Margarine, Gross Margin

30 Sep 2016

School

Department

Course

Professor

Document Summary

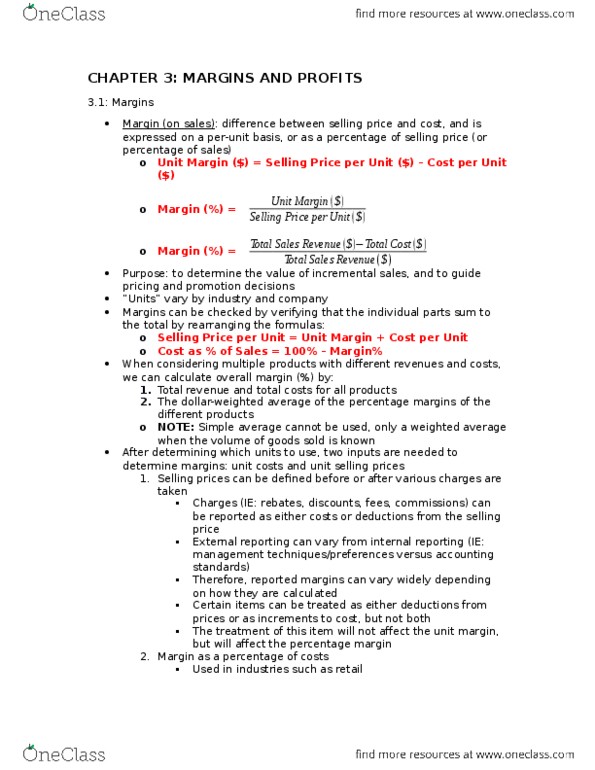

A business can survive only if it makes both a margin and a profit. Margin: the difference between a product"s price and its cost. The contribution margin tells us how much the sale of each unit of that product will contribute to covering a firm"s fixed costs. Expressed as % of selling price or per-unit basis: unit margin ($) = selling price per unit ($) cost per unit ($, margin (%) = unit margin ($) / selling price per unit ($) Or: margin (%) = [total sales revenue ($) total cost ($)] / total sales revenue ($) Every business has its own notion of a unit : example: 64 oz. of cola, a ton of margarine, a bucket of plaster. Particularly in retail, margin is calculated as a percentage of costs instead of selling price. Markup: adding a percentage to costs to calculate selling price. Margin (%) = unit margin ($) / selling price per unit ($)