ADMS 3490 Chapter Notes - Chapter 4: Pension, Job Performance, Fixed Cost

29 Sep 2012

School

Department

Course

Professor

Document Summary

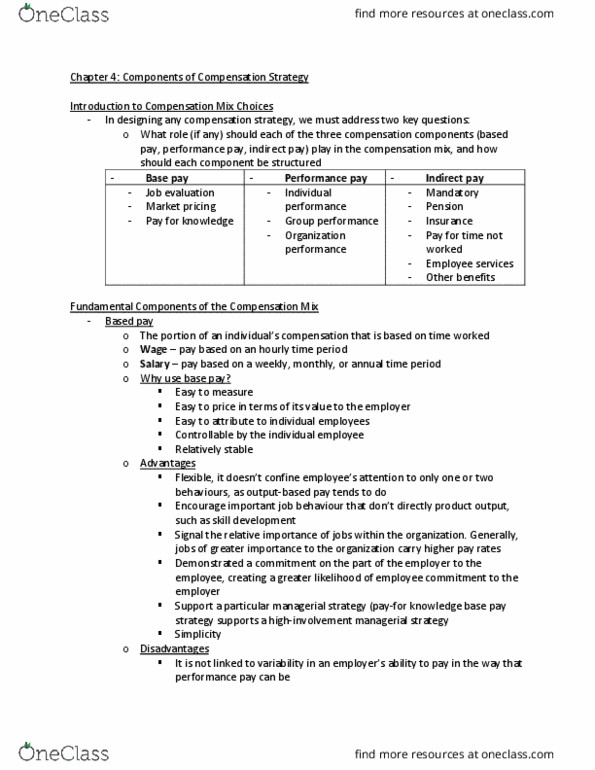

The first strategic decision is about the relative proportions of base pay, performance pay, and indirect pay to include in the compensation mix. Three other choices follow what method(s) should be used for establishing base pay, what type(s) of performance pay(if any) should be provided, and which elements of indirect pay should be included. Base pay job evaluation, market pricing, and pay for knowledge. Performance pays individual performance, group performance, and organization performance. Indirect pay mandatory benefits, pension plan, health and life insurance, pay for time not worked, employee services, and other benefits. Base pay: is the portion of an individual"s compensation that is based on time worked not on the output produced or results achieved. Base pay accounts for 75 to 80 percent of the compensation for a typical employee, performance pay about 5 to 10percent, and indirect pay about 15 percent of the total compensation.