MKT 100 Chapter Notes - Chapter 11: Monopolistic Competition, Pricing Strategies, Oligopoly

28 Feb 2016

School

Department

Course

Professor

1

MKT 100 Full Course Notes

Verified Note

1 document

Document Summary

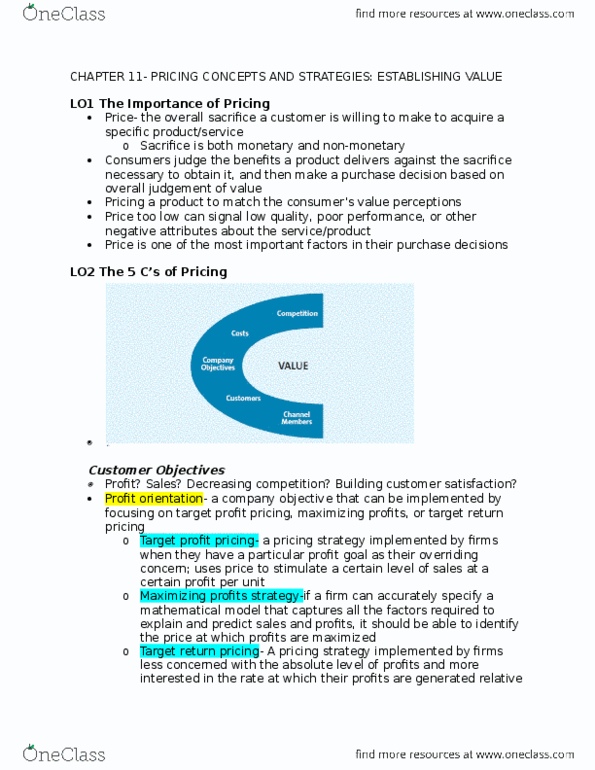

Price: the sacrifice that a consumer is willing to make (monetary- travel costs, taxes, shipping costs or nonmonetary- time) to acquire a specific product/service. Priced too high communicates low value, priced too low communicates low quality. Price is the only element of the marketing mix that generates revenue. Price is an information cue, that is, consumers use the price of a product/service to judge its quality, particularly when they are less knowledgeable about the product/service. Company, objectives, customers, costs, competition, and channel members. Profit orientation: a company objective that can be implemented by focusing on target profit pricing, maximizing profits, or target return pricing. Sales orientation: a company objective based on the belief that increasing sales will help the firm more than will increasing profits. Competitor orientation: a company objective based on the premise that the firm should measure itself primarily against its competition: competitive parity: firms set prices that are similar to those of their major competitors.